Seeing the high cost of a dental crown or root canal can create immediate stress around oral care decisions. Paying monthly insurance premiums often still leads to large out-of-pocket bills, especially when plans restrict dentist choice or delay major treatment.

Greater control over dental costs starts with understanding how different insurance structures affect the final bill at the office. Knowing these categories helps in selecting a plan that actually covers major procedures without unexpected surprises.

In this guide, you will learn about the different types of dental insurance and why the right plan choice truly matters.

Quick Look

PPO Flexibility: These plans offer the widest choice of dentists and allow you to see any licensed provider you prefer.

DHMO Limits: You must use an assigned primary dentist and obtain referrals for any specialized dental work you might need.

Benefit Caps: Many standard plans cap your annual benefits at $1,000, which can be exhausted by just one major procedure.

Waiting Periods: Traditional insurance often makes you wait six to twelve months before covering expensive work like crowns or bridges.

Discount Plans: These are not actually insurance but memberships that provide reduced rates at specific participating dental office locations.

What Are the Main Types of Dental Insurance?

Choosing the right dental coverage requires you to look beyond the monthly price and analyze how the plan actually functions. The way a plan is structured determines which dentists you can visit and how much you pay for a filling. Most people focus on the brand name, but the plan category is what truly controls your out of pocket costs.

You should evaluate these specific categories to find a balance between monthly premiums and the quality of your dental care:

PPO (Preferred Provider Organization)

DHMO (Dental Health Maintenance Organization)

Indemnity (Fee-for-Service) Plans

Discount Dental Plans (Non-Insurance)

Marketplace and Employer Plans

Understanding these core differences is the first step toward getting the dental care your family deserves without any hidden fees.

Are you tired of being told you must wait six months for a root canal while you are in pain? TrueCost Group offers PPO plans with no waiting periods and up to $5,000 in annual coverage for your major work. Get a free quote over text today to access a national network of 85,000 dentists and immediate dental benefits.

PPO Dental Insurance Plans

A Preferred Provider Organization is the most popular choice for families who want the freedom to choose their own dentist. You can visit any provider in the country, but you will save the most money by staying within the network.

How PPO Dental Plans Work

You can see any licensed dentist, but in-network providers offer lower negotiated rates for all of your covered services.

The insurance company pays a set percentage of the bill while you pay the remaining balance through a coinsurance model.

You do not need a referral to see a specialist, like an oral surgeon or a periodontist, for your care.

What PPO Plans Typically Cover

Most PPO plans cover 100% of preventive care like cleanings, exams, and basic X-rays for you and your family.

Basic services like fillings and extractions are usually covered at 80% after you meet your small annual plan deductible.

Major procedures such as crowns, root canals, and dentures are typically covered at 50% up to your annual maximum limit.

Costs to Expect With a PPO Plan

Monthly premiums often range between $30 and $50.

Annual deductibles typically range from $0 to $100.

Annual maximums commonly range between $1,000 and $5,000.

Real Example: PPO Dental in Action

If you need a cleaning, a filling, and a crown, a PPO plan might save you over $1,000 in total. Without insurance, these services could cost $1,500, but with a PPO, your out-of-pocket cost might be only $700.

Pros and Cons of PPO Dental Plans

Pros: Total flexibility to choose your dentist and access to a large national network of over 85,000 providers today.

Cons: Monthly premiums are generally higher than DHMO plans, and you must manage an annual maximum benefit limit each year.

The flexibility of a PPO plan makes it a strong choice for people who value choice and comprehensive dental coverage.

DHMO / HMO Dental Insurance Plans

A Dental Health Maintenance Organization is a lower-cost option that requires you to follow a much more rigid structure. You sacrifice your choice of dentist in exchange for lower monthly premiums and fixed copays for every dental service you receive.

How DHMO Plans Work

You are required to select one primary care dentist from a specific list provided by the insurance company for care.

All of your dental treatments must be coordinated through this primary dentist to be eligible for any insurance payment.

You must obtain a formal referral from your primary dentist before you can visit any specialist for advanced dental work.

What DHMO Plans Cover (and Limit)

These plans focus heavily on preventive care and often include $0 copays for your regular cleanings and dental checkup exams.

While they cover a wide range of services, you might find caps or total exclusions on expensive major dental procedures.

You only have coverage if you stay within the very small network of dentists assigned by the insurance carrier's plan.

Costs to Expect With DHMO Plans

Monthly premiums are very low and can range from $5 to $20 for an individual member in most states.

You usually do not have to pay an annual deductible or worry about a yearly maximum benefit limit for care.

You pay a flat copay for each service, such as $15 for an exam or $300 for a porcelain crown.

Real Example: DHMO Dental in Action

If you need a crown, you might pay a flat $250 copay regardless of what the dentist normally charges the public. This makes your costs very predictable, but you are limited to the few dentists who participate in the DHMO network.

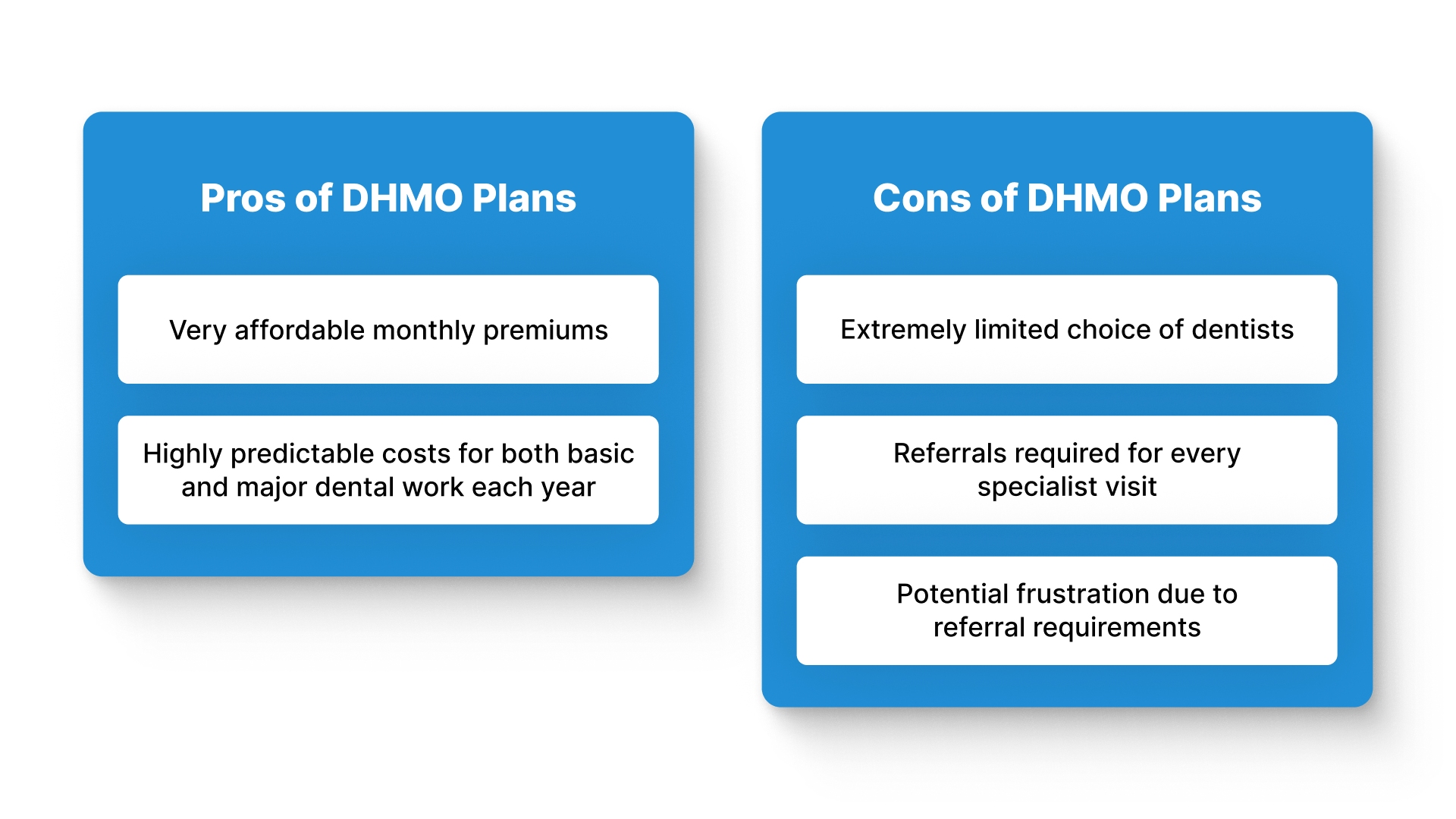

Pros and Cons of DHMO Plans:

Pros: Very affordable monthly costs and highly predictable out-of-pocket expenses for basic and major dental work every year.

Cons: Extremely limited choice of dentists and the frustration of needing referrals for every specialist visit you might require.

Selecting a DHMO plan is a viable strategy if you are on a tight budget and like your assigned dentist.

Indemnity (Fee-for-Service) Dental Insurance

Indemnity plans are a traditional type of coverage that offers the highest level of freedom but involves more personal administrative work. These plans do not use a network, so you can visit any dentist in the world for your dental procedures.

How Indemnity Plans Work

You can visit any dentist you want, and the insurance company will pay a set percentage of the "usual" fees.

There is no network of providers, so you never have to worry about whether a specific dentist is covered or not.

You often have to pay the dentist the full amount upfront and then submit a claim for reimbursement yourself.

Costs and Reimbursement Structure

Monthly premiums for indemnity plans are usually the highest in the market because of the total freedom they provide users.

You will still have to meet an annual deductible and manage a yearly maximum benefit limit for your dental care.

The insurance company only pays based on its own fee schedule, which might be lower than what your dentist charges.

When Indemnity Plans Make Sense

These plans are ideal if you live in a rural area where few dentists participate in traditional PPO or HMO networks.

They are a good fit for people who have a very specific specialist they want to see, regardless of the cost.

Indemnity plans are becoming less common as PPO networks continue to grow and offer more balance for the average consumer.

Discount Dental Plans (Not Insurance)

A discount dental plan is a membership program where you pay an annual fee to access lower rates at participating dentists. It is important to remember that this is not insurance and the company does not pay any of your bills.

How Discount Dental Plans Work

You pay a small annual or monthly membership fee to join a program like Cigna Dental Savings or Aetna Vital.

You present your membership card at a participating dentist's office to receive a discounted rate for your dental services.

There are no claim forms to file, and you pay the dentist directly for the discounted amount at your visit.

What Discount Plans Do and Do Not Cover

You receive a discount on almost every procedure, including preventive, basic, and major services like root canals and dental crowns.

These plans do not have waiting periods, so you can join today and use the discounts at your appointment tomorrow.

There is no annual maximum, but there is also no actual insurance payment to help cover the cost of care.

Cost Example: Discount Plan vs. Insurance:

For a $1,000 root canal, a discount plan might lower the price to $600, which you pay yourself. A PPO plan might pay 80% of the cost, leaving you with a much smaller $200 bill after your deductible.

When a Discount Plan May Be Appropriate:

They are useful for people who have already hit their annual maximum on their primary insurance plan for the year.

Discount plans are a good short-term solution if you need a procedure done immediately and have no other coverage.

Understanding that a discount plan is a savings tool rather than a payment tool will help you avoid financial confusion.

Marketplace Dental Insurance Plans

Marketplace plans are purchased through the federal exchange or state platforms, often alongside your primary health insurance plan for families. These plans must meet certain standards, but they often have limitations that surprise many adults who sign up for them.

How Marketplace Dental Plans Work

You can buy a standalone dental plan or choose a health plan that already has dental benefits built into it.

Most Marketplace dental plans focus heavily on pediatric care because children's dental is considered an "essential" health benefit by law.

You can only enroll during the Open Enrollment Period unless you have a qualifying life event like moving or marriage.

Common Limitations of Marketplace Dental Plans

Many Marketplace options for adults include long waiting periods of six to twelve months for any major dental procedure.

These plans often have lower annual maximums, which do not cover much major dental care.

The networks can be smaller than private PPO plans, making it harder to find a dentist who accepts your coverage.

Who Marketplace Dental Plans Are Best For

These plans are a great choice for families with young children who primarily need preventive care and basic tooth fillings.

They work well for healthy adults who only want coverage for their two annual cleanings and occasional dental checkup exams.

While convenient to buy with health insurance, Marketplace plans often lack the depth needed for significant adult dental work.

Employer-Sponsored Dental Insurance

Many people receive their dental coverage through their job, where the employer pays a portion of the monthly premium for them. This is often the most affordable way to get high-quality PPO coverage for you and your entire family.

How Employer Dental Plans Are Structured

Your employer chooses a specific carrier and plan type, usually offering you a choice between a PPO and DHMO.

The monthly premium is deducted directly from your paycheck, often using pre-tax dollars to save you even more money annually.

Employers often negotiate better rates and higher annual maximums than you can find on the individual insurance market today.

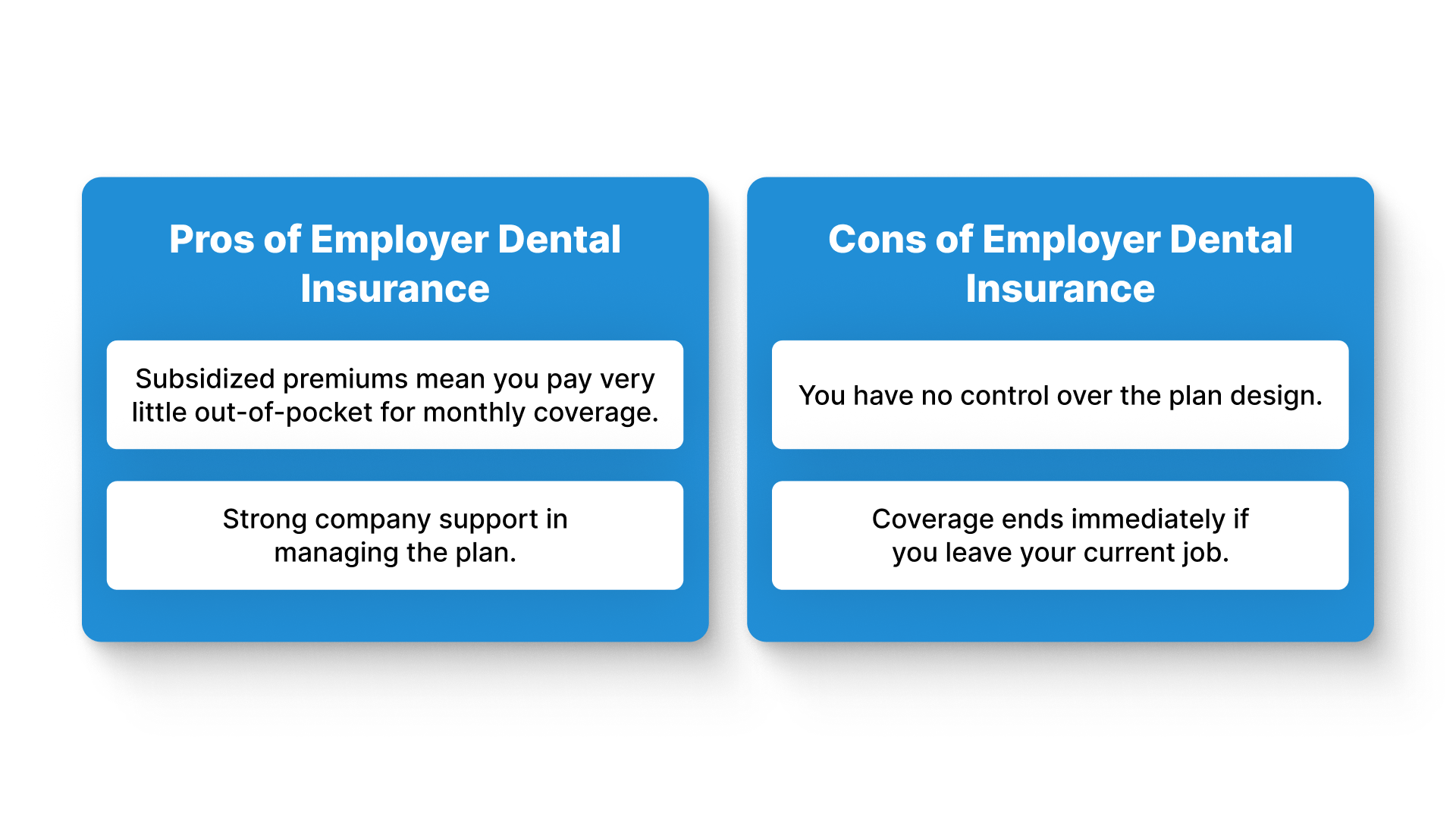

Pros and Cons of Employer Dental Insurance

Pros: Subsidized premiums mean you pay very little out of pocket for your monthly coverage and have strong company support.

Cons: You have no control over the plan design, and your coverage ends immediately if you leave your current job.

What to Check Before Relying on Employer Coverage

Verify if there are any waiting periods for new employees before you can schedule a major procedure like a crown.

Check the annual maximum limit to ensure it is high enough to cover the dental work you expect to need.

Even with employer coverage, you should always compare the benefits to ensure they truly meet your family's unique needs.

Are you frustrated by employer plans that have low limits and narrow networks that exclude your favorite local family dentist? TrueCost Group offers private PPO plans with up to $5,000 in annual coverage and absolutely no contracts or long-term commitments. Get a free quote over text today to access a nationwide network and immediate benefits for major dental procedures.

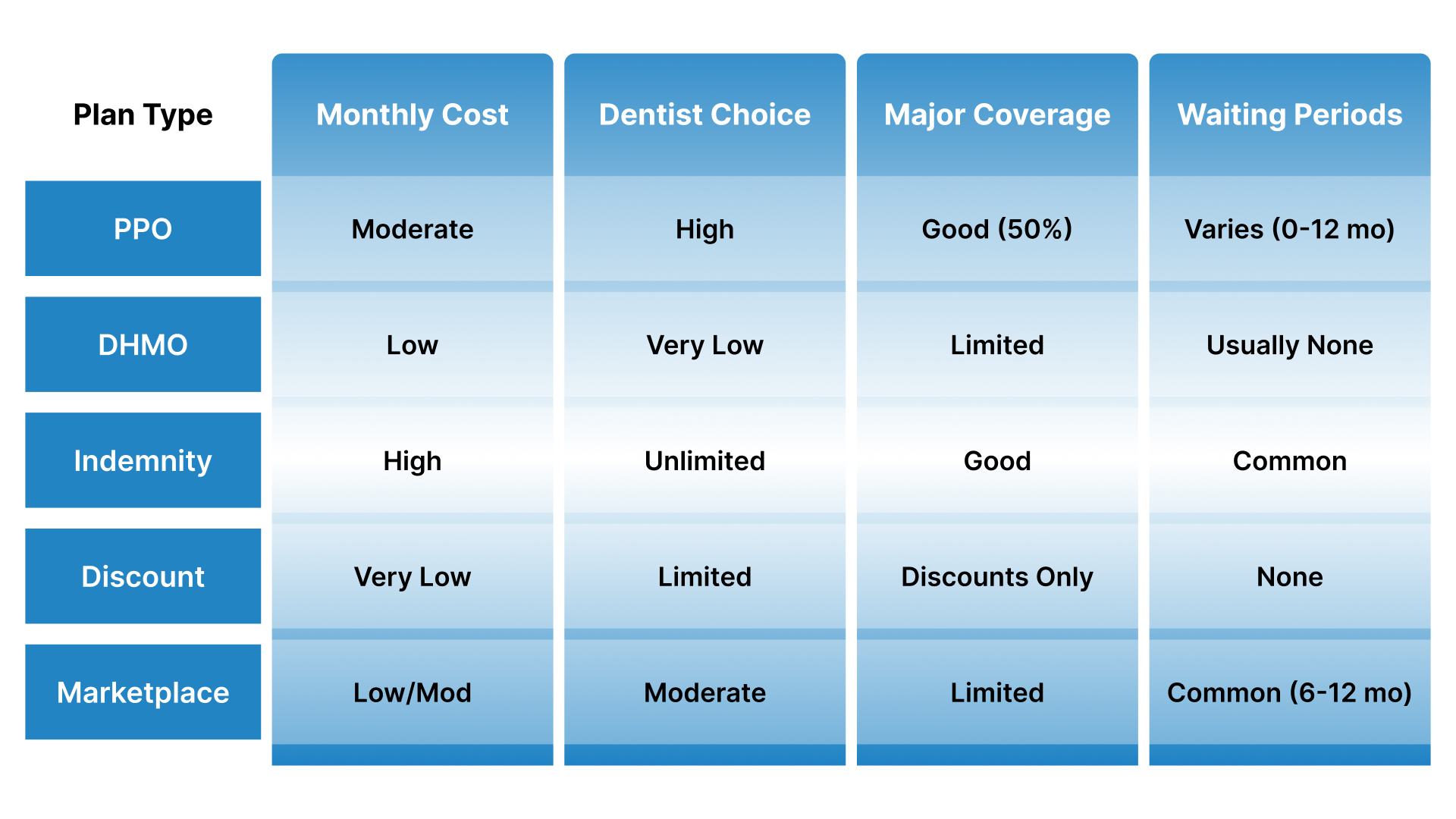

Types of Dental Insurance at a Glance

Choosing between these different types of dental insurance is easier when you see the core factors compared side by side. Each plan type serves a different purpose depending on your health history and your current monthly household budget.

Side-by-Side Comparison Factors:

Monthly Cost: DHMO and discount plans are the cheapest, while PPO and indemnity plans cost more each month for coverage.

Dentist Choice: PPO and indemnity plans offer the most freedom, while DHMO plans restrict you to a specific provider list.

Major Procedure Coverage: PPO plans generally offer the best balance of coverage for expensive work like root canals and crowns.

Waiting Periods: Many private PPO plans through TrueCost Group have no waiting periods, while Marketplace plans often have long delays.

Quick Comparison Table:

Plan Type | Monthly Cost | Dentist Choice | Major Coverage | Waiting Periods |

PPO | Moderate | High | Good (50%) | Varies (0-12 mo) |

DHMO | Low | Very Low | Limited | Usually None |

Indemnity | High | Unlimited | Good | Common |

Discount | Very Low | Limited | Discounts Only | None |

Marketplace | Low/Mod | Moderate | Limited | Common (6-12 mo) |

Selecting the right plan category ensures that you are not overpaying for coverage you do not actually use every year.

How to Choose the Right Type of Dental Insurance

You can simplify your decision by following a step-by-step framework that prioritizes your health needs and your financial situation. Taking the time to analyze your options now will prevent you from facing a massive bill at the dentist's later.

Step-by-Step Decision Framework

Dental History: Look at your past three years of dental visits to see if you typically need major work or just cleanings.

Budget Tolerance: Determine how much you can afford for a monthly premium versus how much you can pay for an emergency.

Provider Preferences: Decide if keeping your current dentist is more important than saving money on your monthly insurance premium cost.

Timeline for Care: If you have a toothache now, you must choose a plan with no waiting periods for immediate dental care.

Questions to Ask Before Enrolling

"What is the exact date my coverage for major procedures like crowns and root canals will actually become active?"

"What is the annual maximum benefit, and is it enough to cover a root canal and a crown this year?"

"Is my current dentist in the network, and what are the out-of-network costs if I choose to stay?"

Asking these questions helps you avoid the common mistakes that lead to denied claims and high out-of-pocket bills.

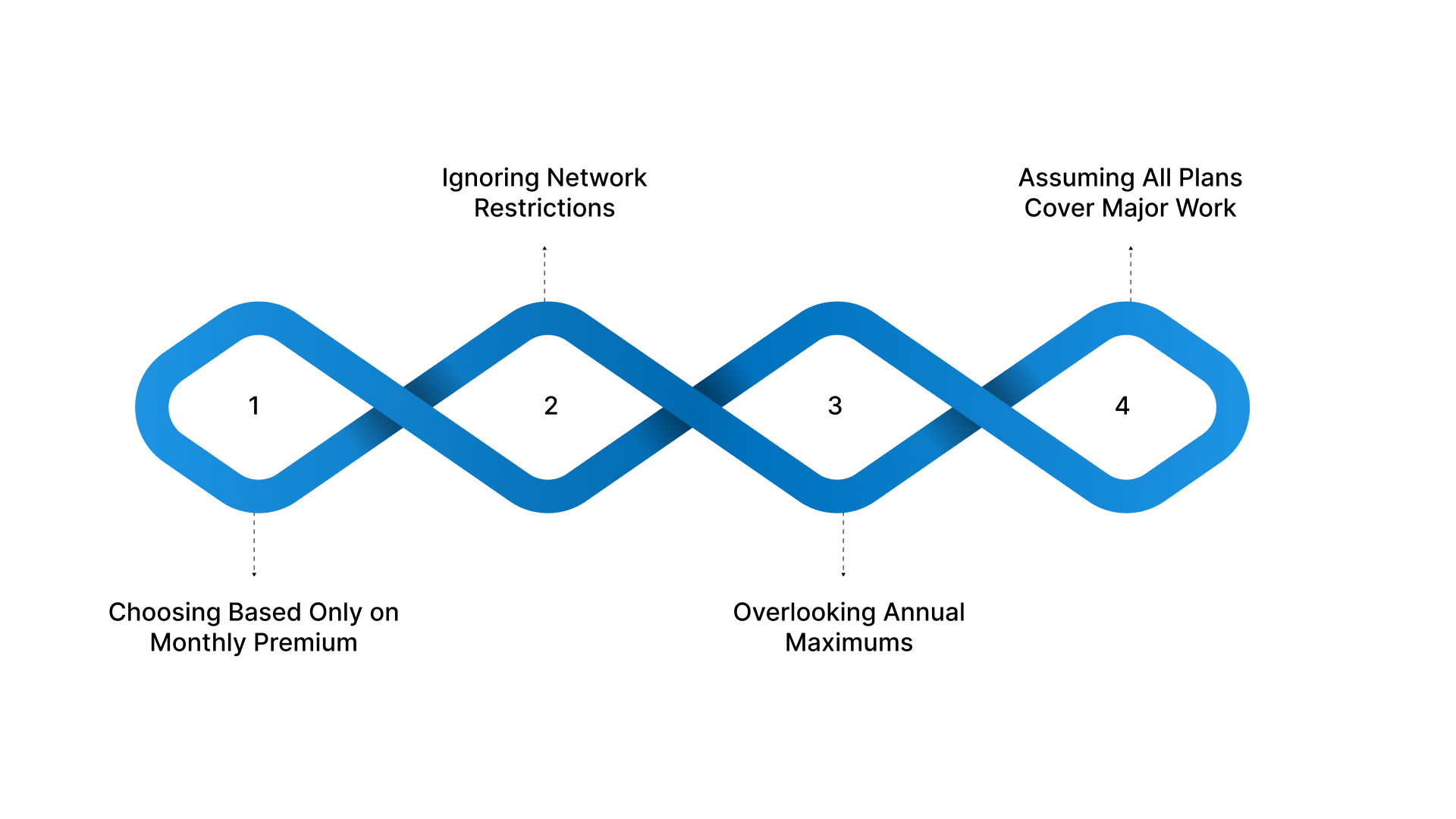

5 Common Mistakes People Make When Choosing Dental Insurance

Many families end up with the wrong coverage because they do not look at the fine print of the policy. Avoiding these common errors will ensure that your dental insurance actually works for you when you need it the most.

Choosing Based Only on Monthly Premium

People often pick the cheapest plan, but then realize it does not cover the major procedure they need right now.

Solution: Compare the total yearly cost, including premiums, deductibles, and the percentage you pay for major dental work.

Ignoring Network Restrictions

Enrolling in a plan without checking the network can force you to leave a dentist you have trusted for years.

Solution: Always use the provider search tool or ask your dentist which specific insurance plans they currently accept for care.

Overlooking Annual Maximums

A plan with a $1,000 limit might seem like enough until you realize one crown can cost $1,200 or more.

Solution: Look for plans with higher annual maximums, like $3,000 or $5,000, to ensure you are fully protected from high costs.

Assuming All Plans Cover Major Work

Some low-cost plans only cover preventive care and leave you paying 100% for anything more complex than a cleaning.

Solution: Read the summary of benefits carefully to ensure that "Major Services" are included in your selected dental plan.

Planning ahead and choosing a plan with clear benefits will give you the confidence to visit the dentist anytime.

TrueCost Group: Your Partner for Immediate and Affordable Dental Care

Finding dental coverage can feel overwhelming on a tight budget, especially with confusing terms and hidden fees. TrueCost Group simplifies the process by offering affordable PPO plans with immediate benefits and clear guidance through simple messaging, so coverage works from day one.

High Annual Limits: Access up to $5,000 in yearly coverage to handle major procedures like root canals, crowns, and dentures.

Immediate Protection: You can skip the six-month waiting periods for major work and start your dental treatment on day one.

National Network Access: Choose from over eighty-five thousand dentists who offer deep discounts to lower your total out-of-pocket costs.

Messenger-First Enrollment: Complete your application through WhatsApp or Facebook Messenger to get covered without filling out long, complex forms.

Month-to-Month Flexibility: Manage your budget with a plan that has no long-term contracts and allows you to cancel at any time.

You can finally stop worrying about the high cost of a healthy smile by choosing a plan designed for life.

Conclusion

Choosing between the different types of dental insurance is the most important step in protecting your family's oral health. Whether you prefer the flexibility of a PPO or the low cost of a DHMO, your choice impacts your wallet.

Remember to prioritize plans with no waiting periods and high annual maximums if you expect to need major dental work soon.

TrueCost Group is here to help you navigate these options with simple, advisor-guided enrollment through the apps you use. We specialize in finding affordable PPO plans that offer immediate benefits so you can visit the dentist with total confidence.

Our goal is to ensure you get the high-quality care you need without the traditional insurance industry confusion.

Get your free quote over text today to see how much you can save on dental care for your family.

FAQs

Q. What is the most common type of dental insurance?

The PPO (Preferred Provider Organization) is the most common type because it offers a balance of flexibility and cost savings. Most people prefer PPOs because they allow you to choose any dentist while still providing significant discounts for staying in-network.

Q. Which dental plan is best for major dental work?

A PPO plan with a high annual maximum and no waiting periods is usually the best choice for major work. These plans provide the highest dollar amount of coverage for expensive procedures like root canals, crowns, bridges, and dentures.

Q. Are discount dental plans worth it?

Discount plans can be worth it if you do not have insurance and need immediate savings on a specific dental procedure. However, they do not pay for your care, so you are still responsible for the entire discounted bill at the office.

Q. Can you switch dental insurance types mid-year?

You generally cannot switch plans mid-year unless you have a qualifying life event like a job change or a move. However, private plans through TrueCost Group offer more flexibility than many employer-sponsored or Marketplace plans you might find today.

Q. What type of dental insurance has no waiting period?

TrueCost Group offers specific PPO plans that have no waiting periods for preventive, basic, or even major dental services. This means your coverage starts on day one, allowing you to get the treatment you need without any long delays.