You probably worry about the high cost of dental work every time you feel a slight toothache begin to develop. A single crown or root canal can easily cost you over a thousand dollars when you pay out of pocket.

Many people skip the dentist because they fear getting a massive bill that they simply cannot afford right now. You deserve a way to protect your teeth and your wallet without dealing with confusing jargon or hidden fees.

Finding the right dental plan allows you to visit a quality dentist while the insurance company pays the bill. Modern dental options provide you with the financial safety net needed to keep your smile healthy and bright.

In this guide, you will learn everything about dental insurance and discover how these flexible plans work for your family.

Quick Look

Total Flexibility: You can choose any dentist you want, though visiting in-network providers saves you the most money.

Immediate Care: Many PPO plans offered through TrueCost Group feature day-one benefits with absolutely no waiting periods.

Preventive Focus: Routine cleanings and exams are usually covered at one hundred percent to stop problems before they start.

High Value: You get access to a national network of over eighty-five thousand dentists for less than one dollar daily.

No Long-Term Risk: These plans typically operate on a month-to-month basis with no restrictive long-term contracts or commitments.

What Is Dental Insurance

Dental insurance is a specific type of health coverage designed to pay a portion of your professional dental costs. It functions by spreading the financial risk of expensive treatments across a large group of people paying monthly fees.

Unlike paying cash, insurance provides you with pre-negotiated lower rates that make both routine and emergency care much more affordable.

Importance of Dental Insurance

Managing High Costs: A monthly plan prevents you from facing a thousand-dollar bill for a single crown or root canal.

Prioritizing Prevention: Insurance encourages regular visits, which catch small cavities before they turn into painful and expensive dental emergencies.

Lowering Lifetime Spending: Insured individuals typically pay significantly less for dental care over their lifetime compared to those paying cash.

Understanding these benefits is the first step toward choosing a plan that fits your current budget and lifestyle.

Do you avoid the dentist because you fear a surprise bill for a root canal or an expensive crown? TrueCost Group offers PPO plans with no waiting periods and up to $5,000 in annual coverage for major work. Get a free quote over text today to access 100% free exams and a national network of dentists.

Types of Dental Insurance Plans

Not all dental insurance works the same way, so you must choose the structure that fits your specific needs. The most common plan types offer different levels of flexibility regarding which dentists you are allowed to visit:

PPO Dental Insurance

PPO plans offer the most flexibility because you can visit any licensed dentist nationwide. You save the most money when visiting in-network dentists, but partial coverage still applies outside the network.

Example:

A routine cleaning costs $180 without insurance. With a PPO plan, you pay $0 for cleanings, and a $1,200 root canal may cost you only $300–$500 after insurance.

HMO Dental Insurance

HMO plans require you to select one primary dentist from a limited list and get referrals for specialists. Monthly premiums are usually lower, but provider choice is restricted.

Example:

You pay $20 per month for an HMO plan. Cleanings cost $0, and a filling costs $40, but a $1,200 crown may not be covered at all.

Discount Dental Plans

Discount dental plans are memberships, not insurance, and provide reduced cash prices for services. You pay the dentist directly, and no claims are filed.

Example:

A crown priced at $1,400 may drop to $1,050 with a discount plan. You pay the full amount yourself, with no insurance reimbursement.

Choosing a plan type is easier when you see how the actual payment and billing cycle works step-by-step.

How Dental Insurance Works in 4 Simple Steps

Dental insurance functions as a partnership between you, your dentist, and the insurance company to share your healthcare costs. The process follows a predictable cycle that ensures you are covered from the moment you sign up until payment:

Step 1: Paying Your Monthly Premium

You pay a set amount every month to keep your dental coverage active and ready for use when needed.

Plans with higher premiums usually offer better coverage for major work and have lower out-of-pocket costs for the patient.

Step 2: Visiting a Dentist

You schedule an appointment with a dentist and provide your insurance member ID card to the office staff members.

Visiting an in-network provider ensures you receive the deepest discounts and that the office handles all your insurance paperwork.

Step 3: How Claims Are Filed and Processed

Your dental office sends an itemized bill, called a claim, to the insurance company after your treatment is finished.

The insurance company reviews the treatment to ensure it is covered under your plan and follows all clinical guidelines.

Step 4: How Insurance Pays and You Share Costs

The insurer pays its portion directly to the dentist based on the coinsurance percentages listed in your specific policy.

You are responsible for paying any remaining balance, which might include your annual deductible or your specific coinsurance percentage.

Once you know how the system moves, you can look at the specific categories of care that insurers cover.

What Dental Insurance Covers

Most dental insurance plans group treatments into three main categories to determine how much the insurance company will pay. Knowing these categories helps you predict your costs before you even walk into the dental office for your appointment:

Preventive Care

This category includes routine cleanings, oral exams, and bitewing X-rays, which are essential for maintaining your oral health. Most plans cover these services at one hundred percent because they prevent much more expensive problems from developing later.

Basic Dental Services

Basic care covers common repairs like silver or tooth-colored fillings and simple extractions of a damaged tooth. These services are typically covered at around eighty percent, meaning you only pay a small portion of the total bill.

Major Dental Services

Major care includes complex work like porcelain crowns, root canals, bridges, and full or partial sets of dentures. Because these procedures are expensive, insurance usually covers about fifty percent of the cost, while you pay the other half.

Each of these categories is affected by specific insurance terms that determine exactly when and how coverage applies.

Key Dental Insurance Terms You Must Understand

Navigating dental insurance 101 requires you to understand a few specific terms that impact your final out-of-pocket costs.

Learning these definitions will remove the confusion and fear often associated with reading an insurance policy or a bill:

Deductible: This is a fixed dollar amount you must pay out of pocket before the insurance company starts paying for care. Most dental deductibles are small, often ranging between fifty and one hundred dollars per person for the entire year.

Coinsurance and Copayments: Coinsurance is the percentage of the bill you share with the insurer, such as paying 20% for a filling. A copayment is a flat fee you pay for a specific service, like $20 for every dental exam.

Annual Maximum: This is the most money an insurance company will pay for your dental care during a single calendar year. Once you hit this limit, you must pay the full price for any additional work until your plan resets.

Waiting Periods: A waiting period is a set amount of time you must be enrolled before the insurer pays for work. Many plans have six-month waits for fillings and twelve-month waits for major work like crowns or root canals.

Understanding these terms helps you evaluate the true value of a plan beyond just the monthly premium price.

How Much Does Dental Insurance Cost, and Is It Worth It

You can typically find quality PPO dental insurance plans for a monthly premium ranging between $0 and $50. While paying for insurance adds a monthly expense, it protects you from sudden thousand-dollar bills for unexpected dental emergencies.

Insurance is almost always worth the cost if you use your two free cleanings and need occasional fillings.

Comparing these costs to your personal dental history will help you choose the most effective plan for you.

How to Choose the Right Dental Insurance Plan

Selecting a plan does not have to be a stressful experience if you follow a simple and organized checklist. You should focus on finding a balance between the monthly premium and the level of coverage you actually need:

Step-by-Step Plan Selection Checklist

Confirm that your favorite local dentist is part of the plan's network to ensure you get the best rates.

Review the coverage percentages for major work if you know you will need a crown or bridge soon.

Check for high annual maximums so you do not run out of insurance money during a busy dental year.

Look for plans with no waiting periods if you need to start your dental treatment immediately after you enroll.

Questions to Ask Before Enrolling

"Does my coverage for major procedures like root canals start on the very first day of my new plan?"

"Are there any specific exclusions for pre-existing conditions like missing teeth that I should know about before signing?"

"Can I manage my enrollment and ask questions through a simple messaging app like WhatsApp or Facebook Messenger?"

By asking the right questions, you can avoid the common errors that lead many people to regret their choice.

Do you need major dental work right now but cannot wait six months for your insurance to start paying? TrueCost Group specializes in PPO plans with day-one major coverage and no long-term contracts to hold you back. Get a free quote over text today to see how much you can save on root canals, crowns, and dentures.

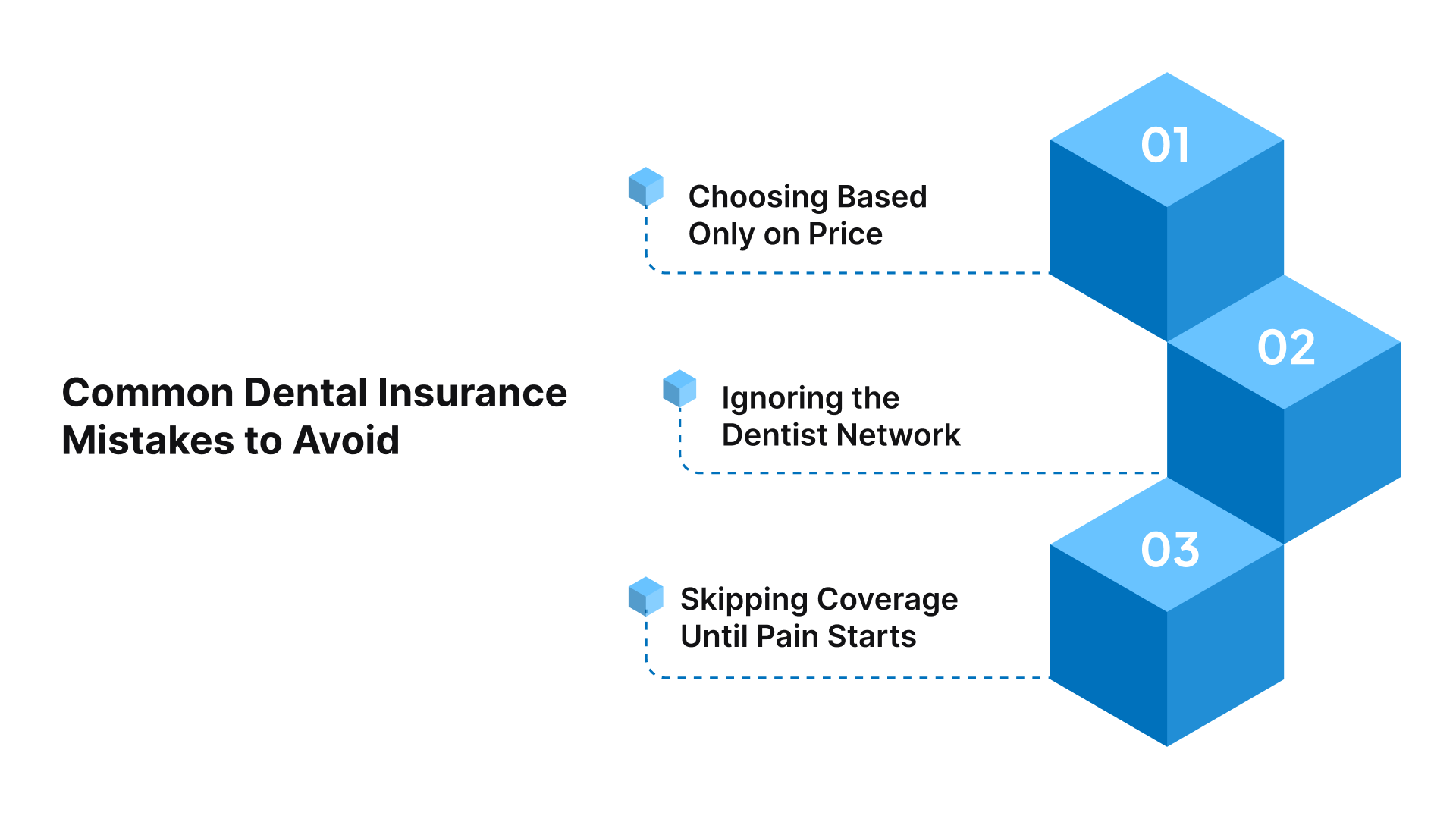

Common Dental Insurance Mistakes to Avoid

Many people miss out on the full value of their benefits because they make decisions based on incomplete information. Avoiding these common pitfalls will ensure that your dental insurance works effectively for your health and your monthly budget:

Choosing Based Only on Price

Low-cost plans often include high deductibles, limited coverage, or long waiting periods that delay needed care. Focusing only on the monthly premium can lead to higher out-of-pocket costs later.

Solution:

Compare coverage percentages, annual maximums, waiting periods, and included services alongside the monthly premium to evaluate total value.

Ignoring the Dentist Network

Seeing an out-of-network dentist usually means paying higher rates that insurance does not fully cover. Many people assume all dentists accept their plan, which leads to unexpected bills.

Solution:

Confirm your dentist’s network status through the insurer’s directory or advisor before scheduling any appointment.

Skipping Coverage Until Pain Starts

Waiting until pain appears often results in uncovered major procedures due to waiting periods. This approach turns preventable issues into costly emergencies.

Solution:

Maintain continuous coverage and use preventive benefits regularly to identify problems early and reduce long-term costs.

Finding a plan that avoids these mistakes is much easier when you have the right partner to guide you.

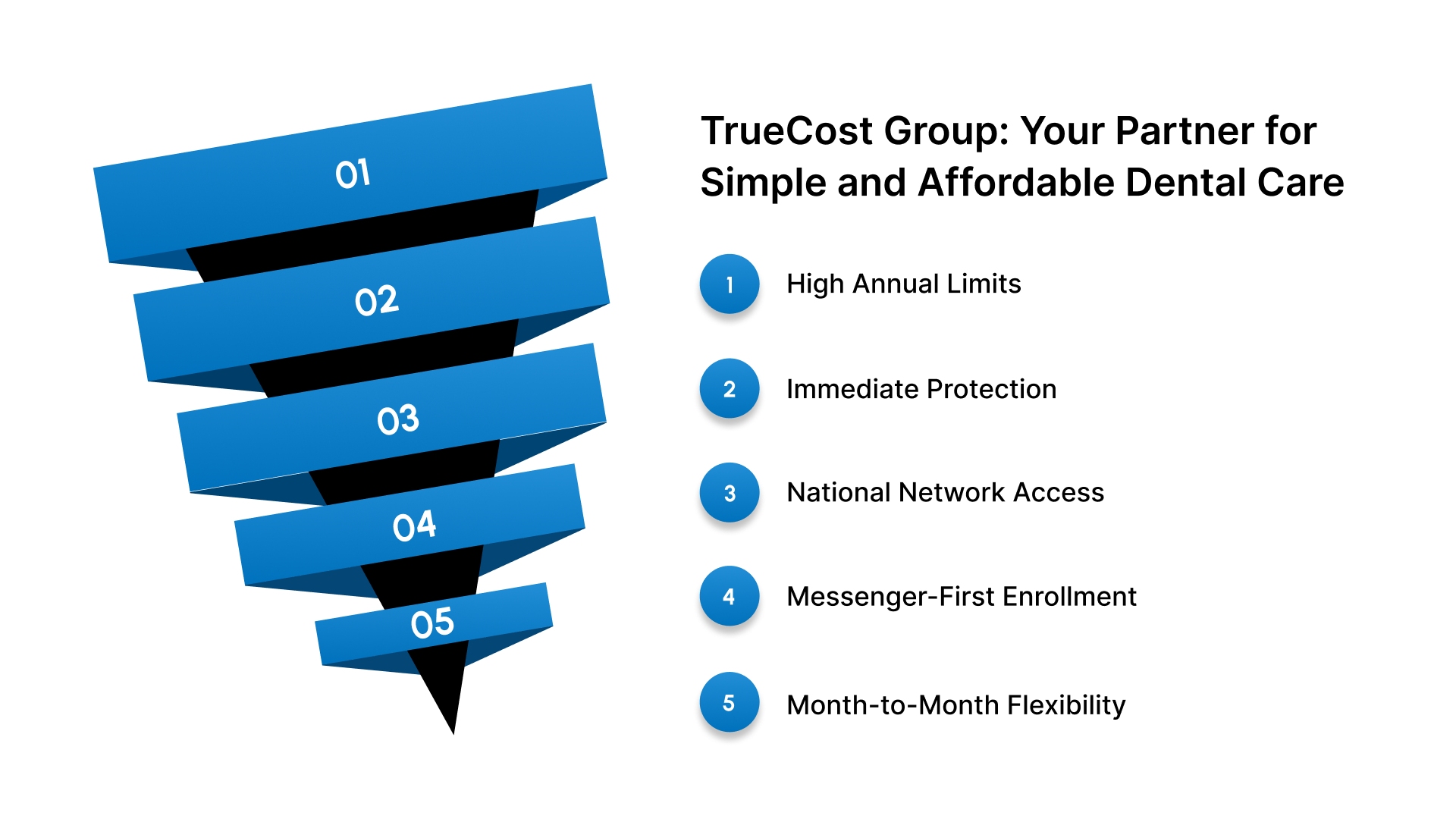

TrueCost Group: Your Partner for Simple and Affordable Dental Care

Finding the right dental coverage can feel overwhelming when you are working within a tight budget. Insurance terms and high-limit plans may seem confusing or unreliable. Many families stay uninsured because enrollment feels slow and unclear.

TrueCost Group removes these barriers by helping you access high-limit PPO dental plans with immediate benefits. You receive expert guidance through simple messaging so you feel protected before your next dental visit.

High Annual Limits: Access up to $5,000 in yearly coverage to handle major procedures like root canals, crowns, and dentures.

Immediate Protection: You can skip the six-month waiting periods for major work and start your dental treatment on day one.

National Network Access: Choose from over eighty-five thousand dentists who offer deep discounts to lower your total out-of-pocket costs.

Messenger-First Enrollment: Complete your application through WhatsApp or Facebook Messenger to get covered without filling out long, complex forms.

Month-to-Month Flexibility: Manage your budget with a plan that has no long-term contracts and allows you to cancel at any time.

You can finally stop worrying about the high cost of a healthy smile by choosing a plan designed for life.

Conclusion

Dental insurance teaches us that having the right plan is the best way to prevent expensive dental bills. By focusing on preventive care and choosing a PPO plan with a large network, you protect your overall health.

Remember that plan structure and immediate benefits are much more important than just the brand name of the insurer.

TrueCost Group is dedicated to helping individuals and families find affordable dental coverage that works from the very first day. We remove the confusion of insurance by providing human-led guidance through the messaging apps you already use every day. Our goal is to ensure you feel confident and protected every time you visit a dentist for your care.

Get your free quote over text today to see how much you can save on dental care for your family.

FAQs

Q. Is Dental Insurance Required?

Dental insurance is not legally required for adults, but it is highly recommended to manage the high costs of care. Without a plan, you are responsible for the full price of every cleaning, filling, or emergency procedure you receive.

Q. Can You Use Dental Insurance Immediately?

Many plans have waiting periods, but you can find PPO options through TrueCost Group that offer immediate day-one benefits. These plans allow you to get cleanings or even major work done right after your enrollment is officially processed.

Q. What Happens If You Exceed Your Annual Maximum?

If you go over your annual limit, you must pay the full discounted rate for any additional dental work. You should work with your dentist to schedule expensive treatments across two different years to stay within your limits.

Q. Does Dental Insurance Cover Emergencies?

Most dental insurance plans provide coverage for emergencies like a knocked-out tooth or a sudden and painful tooth infection. These visits are usually classified as basic or major services depending on the type of treatment the dentist performs.

Q. Can You Have More Than One Dental Insurance Plan?

You can legally have two dental plans, which is a process called coordination of benefits, to lower your costs. This is often common for families where both spouses have their own separate dental insurance through their different employers.