Introduction

Your child's dentist recommends braces, and you're suddenly facing a $5,000-$7,000 bill. Or your partner needs an emergency crown, adding another $1,200-$1,500 to your expenses. Without adequate dental insurance, families can quickly rack up thousands in unexpected dental costs.

National dental expenditures hit $189 billion in 2024—a 4% increase from the previous year. With children requiring regular preventive care plus potential orthodontics, choosing the right dental insurance is a critical financial decision.

These rising costs create real barriers. Despite widespread coverage availability, 13% of Americans still can't afford the dental care they need.

This guide helps you understand what coverage your family actually needs and how to evaluate plans based on your specific situation—not just premiums.

Key Takeaways

- Family plans cost $30-$100/month with preventive care at 100%, basic at 70-80%, major at 50%

- Annual maximums of $1,500-$2,000 per person cap yearly payouts

- Orthodontic benefits cover 50% up to $1,000-$2,000 per child after 12-24 month wait

- Check if your dentist is in-network before enrolling to avoid surprise costs

- Compare total yearly costs against expected dental expenses to verify savings

What is Family Dental Insurance?

Family dental insurance is coverage designed to reduce out-of-pocket costs for dental care for multiple family members under one plan.

Rather than paying full price for cleanings, fillings, crowns, or braces, you pay a monthly premium in exchange for the insurer covering a percentage of these costs.

Basic Structure:

- Monthly premiums typically range from $30-$100 for families

- Deductibles of $50-$100 per person before coverage begins

- Coverage percentages that vary by service type (preventive, basic, major)

- Annual maximums of $1,500-$2,000 per person

Most family plans cover two adults and dependent children up to age 26. Pricing increases based on the number of covered members.

According to the National Association of Dental Plans, Dental PPO plans average $41.76 monthly for individuals, with family rates scaling proportionally.

Key Coverage Categories Families Should Understand

Dental insurance divides services into three or four tiers, each with different coverage levels and waiting periods. Understanding this structure helps you predict actual costs.

Preventive Care (Tier 1)

Covered services:

- Routine cleanings (usually 2 per year)

- Exams and X-rays

- Fluoride treatments for children

- Sealants

Most plans cover preventive care at 100% with no waiting period and no deductible. This makes it the highest-value benefit for families with children who need regular checkups.

Even if you only use preventive services, you're getting substantial value—two cleanings and exams cost approximately $406 annually without insurance.

Basic Procedures (Tier 2)

This tier covers:

- Fillings for cavities

- Simple extractions

- Emergency pain relief

- Non-surgical periodontal treatments

Typical coverage is 70-80% after deductible, with waiting periods of 0-6 months depending on the plan. A filling averages $226, meaning you'd pay roughly $45-$68 out-of-pocket with 80% coverage.

Major Procedures (Tier 3)

Major work includes:

- Crowns ($1,399 average)

- Bridges

- Dentures

- Root canals

- Surgical extractions

- Implants (often excluded)

Coverage is typically 50-60% after deductible, with waiting periods of 6-12 months. This is the most important category to evaluate if you expect needing major work.

With 50% coverage on a $1,400 crown, you'll still pay $700 out-of-pocket—plus this expense counts toward your annual maximum.

Orthodontic Coverage (Often Separate)

Orthodontic coverage for braces and aligners is often sold as an add-on or included in comprehensive plans with separate limits.

Coverage is typically 50% up to a lifetime maximum of $1,000-$2,000 per child, with 12-24 month waiting periods.

Critical detail: With average metal braces costing $6,343 in 2024, even maximum insurance coverage of $2,000 leaves families paying $4,343 out-of-pocket. Adult orthodontic coverage is rare.

What to Consider When Choosing the Best Dental Insurance for Your Family

The "best" plan isn't the one with the lowest premium—it's the one that provides the most value based on your anticipated dental care needs. Balance these six factors against your family's specific situation.

Annual Maximum Limits

Annual maximums typically range from $1,000-$3,000 per person and represent the most the insurance will pay for your care each year.

Research shows that 73% of PPO plans offered annual maximums of $1,500 or more in 2024, yet the percentage of enrollees hitting these caps nearly doubled to 2.9%.

Calculate potential expenses for your family:

- 2 children needing routine care: ~$800

- 1 parent needing a crown: $1,400

- Total: $2,200 (could exceed a $1,000 per-person maximum)

Look for plans with at least $1,500-$2,000 per person annual maximums, or higher if you anticipate major work.

Waiting Periods for Different Service Levels

Waiting periods are the time between when your coverage starts and when you can actually use benefits for certain services.

Most plans follow this timeline:

- Preventive care: 0 months (immediate)

- Basic procedures: 0-6 months

- Major work: 6-12 months

- Orthodontics: 12-24 months

If your child needs braces within six months, a 12-month orthodontic waiting period won't work for you. Many carriers waive waiting periods if you can prove 12 months of continuous prior coverage.

Network Size and Provider Access

PPO vs. HMO plans:

| Feature | PPO Plans | HMO Plans |

|---|---|---|

| Network size | Larger (89% of market) | Smaller, restricted |

| Out-of-network options | Yes, at reduced coverage | No coverage |

| Referrals required | No | Yes, from primary dentist |

| Average monthly premium | $41.76 individual | $15.14 individual |

| Best for | Families wanting flexibility | Budget-focused families |

Check if your current family dentist is in-network before enrolling. Verify that pediatric dentists and orthodontists participate in the network if you have children. PPO plans typically offer better value for families who want choice in providers.

Orthodontic Coverage Terms and Limitations

If you have children who may need braces, orthodontic coverage should be a primary decision factor.

Key details to verify:

- Lifetime maximum: Typically $1,000-$2,000

- Coverage percentage: Usually 50%

- Waiting periods: Often 12-24 months

- Age limits: Frequently restricted to dependents under age 19

If braces cost $5,000 and insurance covers $1,500, you'll still pay $3,500 out of pocket.

Approximately 7.4% of U.S. children aged 8-17 were in active orthodontic treatment in 2022, making this a common family expense.

Deductibles and Out-of-Pocket Cost Structure

Deductibles are typically $50-$100 per person annually, with some plans having family deductibles (e.g., $150 for the whole family regardless of how many members use services).

Two cost-sharing structures exist:

- Copays (flat fees per visit): Common in HMOs. You pay $25 per cleaning, for example.

- Coinsurance (percentage-based): Common in PPOs. You pay 20% of the procedure cost after meeting your deductible.

Calculate total annual costs including premiums, deductibles, and estimated coinsurance based on anticipated care needs.

Premium Costs vs. Coverage Value

Family dental insurance premiums typically range from $30-$100 per month depending on coverage level and family size. Don't choose solely based on lowest premium.

Consider this comparison:

- Plan A: $35/month ($420/year) with $1,000 annual maximum

- Plan B: $65/month ($780/year) with $2,500 annual maximum

If your family needs $2,000 in dental work, Plan B provides $1,220 more in potential coverage for just $360 more in premiums. That's a net gain of $860.

If premiums are $50/month ($600/year) and you anticipate $2,000 in dental expenses, insurance covering 70-80% could save you $600-$800 annually while protecting against unexpected costs.

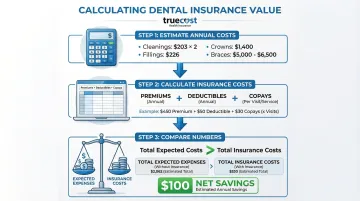

How to Calculate If Dental Insurance is Worth It for Your Family

Dental insurance isn't always the best financial choice for every family. If your household maintains excellent dental health and only needs preventive care, paying out-of-pocket might cost less than annual premiums.

Three-step calculation framework:

- Estimate annual dental costs:

- Routine cleanings for each family member: $203 × 2 visits × family size

- Anticipated fillings: $226 each

- Major work (crowns, root canals): $1,400-$2,700 each

- Orthodontics: $5,000-$6,500 for braces

Once you've estimated your family's dental expenses, calculate what insurance would actually cost you:

- Calculate total insurance costs:

- Annual premiums: Monthly premium × 12

- Deductibles: Per-person or family deductible

- Estimated copays/coinsurance: Based on coverage percentages

Now compare these figures to see your actual savings potential:

- Compare the numbers:

- Expected dental expenses: $1,500

- Insurance costs: $600 premiums + $300 deductibles/copays = $900 total

- Insurance covers: $1,000 of expenses

- Net result: You save $100 while gaining protection against unexpected costs

Dental insurance makes sense for: families with children needing regular care, anyone anticipating major dental work like crowns or root canals, and those who prefer predictable monthly expenses over surprise bills.

You might skip it if: you're a healthy adult without children who maintains excellent dental health, or your family only needs basic cleanings twice a year—in which case dental savings plans may offer better value.

Common Mistakes Families Make When Choosing Dental Insurance

These three mistakes cost families thousands in unnecessary expenses or leave them without coverage when they need it most.

Focusing Only on Monthly Premium

The cheapest monthly premium often comes with high deductibles, low annual maximums, or long waiting periods that reduce actual value.

A $30/month plan with a $1,000 annual maximum provides less protection than a $60/month plan with a $2,500 maximum if your family needs significant dental work. Calculate total annual costs and potential benefits, not just the premium.

Ignoring Waiting Periods When Immediate Care is Needed

Enrolling in a plan with a 12-month waiting period for major work won't help if your child needs a crown in three months. Most plans impose 6-12 month waiting periods on major procedures to prevent adverse selection.

If you have immediate or near-term dental needs:

- Look for plans with no waiting periods or shorter waiting periods

- Ask if the carrier waives waiting periods with proof of prior coverage

- Consider paying out-of-pocket for urgent work while waiting periods expire

Not Verifying Provider Networks Before Enrolling

Discovering your family dentist isn't in-network after enrollment forces you to switch providers or pay significantly higher out-of-network costs.

Out-of-network dentists can balance bill you for the difference between their full fee and what insurance pays. Use the insurance company's provider directory tool before purchasing to confirm your preferred dentists participate. Verify that pediatric dentists and orthodontists are also in-network.

Frequently Asked Questions

What is the average cost of dental insurance for families?

Family dental insurance premiums typically range from $30-$100/month depending on coverage level and family size. Total annual costs including deductibles and copays typically range from $800-$2,500 for a family of four.

What is the best dental insurance for families?

The "best" plan depends on your family's specific needs. Look for plans with at least $1,500 annual maximums per person, orthodontic coverage for children, waiting periods under 6 months for basic procedures, and a strong network of family dentists. PPO plans typically offer the most flexibility.

Is dental insurance worth it for families?

Dental insurance is typically worth it for families with children needing regular preventive care, anyone anticipating major dental work, or families seeking financial predictability. It may not be worthwhile for families with excellent dental health who only need basic cleanings, as out-of-pocket costs may be lower than annual premiums.

Does dental insurance cover braces for children?

Many comprehensive dental plans include orthodontic coverage, typically paying 50% of costs up to a lifetime maximum of $1,000-$2,000 per child after a 12-24 month waiting period. With average braces costing $6,343, expect to pay $4,000-$5,000 out-of-pocket even with insurance.

Can I buy dental insurance outside of Open Enrollment?

Yes. Standalone dental insurance can typically be purchased year-round without waiting for Open Enrollment periods. However, if you're purchasing pediatric dental coverage through the ACA marketplace, you may need to enroll during Open Enrollment unless you qualify for a Special Enrollment Period.

Should families choose a PPO or HMO dental plan?

Most families benefit from PPO plans due to larger provider networks, flexibility to see specialists like orthodontists without referrals, and out-of-network coverage options. PPO plans account for 89% of the commercial dental market. However, HMO plans can be a good budget option for families willing to stay within a smaller network and who prioritize lower premiums over provider choice.

Need help finding the right health coverage for your family? TrueCost Group specializes in helping families navigate ACA marketplace plans and Medicare Advantage options that include supplemental dental benefits. Many families qualify for comprehensive coverage starting at $0-$50/month. Call 1-888-788-8285 to speak with a licensed advisor about your options—no obligation, no hold times.