Frustration often sets in when a primary dental insurance plan barely covers the cost of a necessary major procedure. Many people reach their annual benefit limit quickly and face large out-of-pocket expenses for additional care. A single crown or root canal can easily consume an entire yearly allowance in one visit.

Adding a second layer of coverage can help reduce costs when the first plan falls short. Understanding how dual coverage works allows families to maximize benefits and coordinate payments between insurers. This approach helps manage high dental bills while maintaining consistent preventive and restorative care.

In this guide, you will learn the rules of secondary dental insurance and how to manage multiple active plans.

Quick Look

Dual Coverage: You can legally have two dental plans, which is a process formally known as coordination of benefits.

Payment Limits: Your total reimbursement from both plans cannot exceed the actual amount your dentist charged for the service.

Order of Filing: The primary plan always pays first, followed by the secondary plan covering the remaining eligible balance.

The Birthday Rule: This rule determines which parent's plan is primary for children based on whose birthday falls earlier.

Cost Efficiency: Secondary insurance is most helpful when you expect high dental costs that exceed your primary plan limits.

What Is Secondary Dental Insurance?

Secondary dental insurance is a second policy that helps pay for dental costs after your primary plan reaches its limit. It does not replace your main insurance but works alongside it to reduce your total out-of-pocket medical expenses.

This coverage is common for families where both spouses have dental benefits through their own separate employer-sponsored plans.

Understanding the order in which these plans pay is the first step toward using your dual coverage effectively today.

Are you tired of paying high bills because your current plan has a low annual limit or long waits? TrueCost Group offers PPO plans with no waiting periods and up to $5,000 in annual coverage for major work. Get a free quote over text today to see how our national network can help your family save.

How Secondary Dental Insurance Works in 3 Steps

Coordinating two dental plans involves a specific set of rules to ensure that payments are calculated and distributed correctly. You must follow a standard process so the insurance companies can communicate and settle your dental claims without any delays.

This system ensures that your benefits are applied in the right order to maximize your total yearly savings:

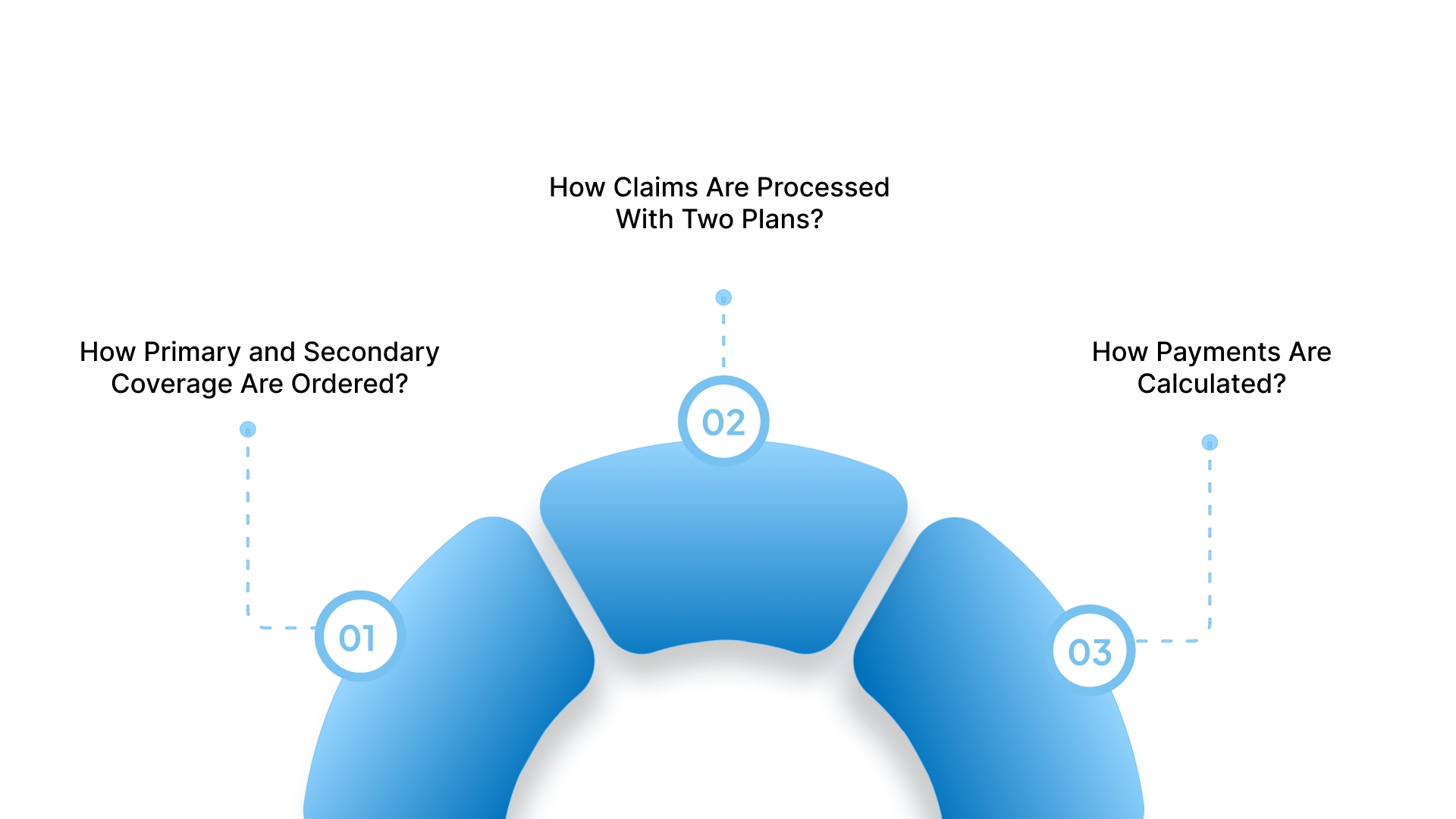

Step 1: How Primary and Secondary Coverage Are Ordered

The plan you have through your own employer is almost always considered your primary dental insurance coverage.

A plan where you are listed as a dependent, such as a spouse's policy, serves as your secondary coverage.

The birthday rule applies to children, making the plan of the parent whose birthday comes earlier in the year primary.

Step 2: How Claims Are Processed With Two Plans

Your dentist submits the initial claim to the primary insurance company to determine their specific portion of the payment.

Once processed, the primary insurer issues an Explanation of Benefits that shows exactly what they covered for the treatment.

The secondary insurer receives the primary EOB and the original claim to calculate any additional benefits they will pay.

Step 3: How Payments Are Calculated

The primary plan pays its standard percentage for the procedure based on their specific network rates and policy rules.

The secondary plan reviews the remaining balance and applies its benefits to cover some or all of that amount.

Coordination of benefits rules prevent you from receiving more money than the dentist actually billed for your dental care.

For example, a dental procedure costs $500, and your primary insurance plan pays 60%. Your primary plan pays $300, leaving you with a remaining balance of $200 for the work.

Your secondary plan might cover 80% of that remainder, which adds another $160 in benefits. Your final out-of-pocket cost is reduced to only $40 because the two plans worked together for you.

Knowing how the payments are split helps you understand exactly what types of dental services are covered by multiple plans.

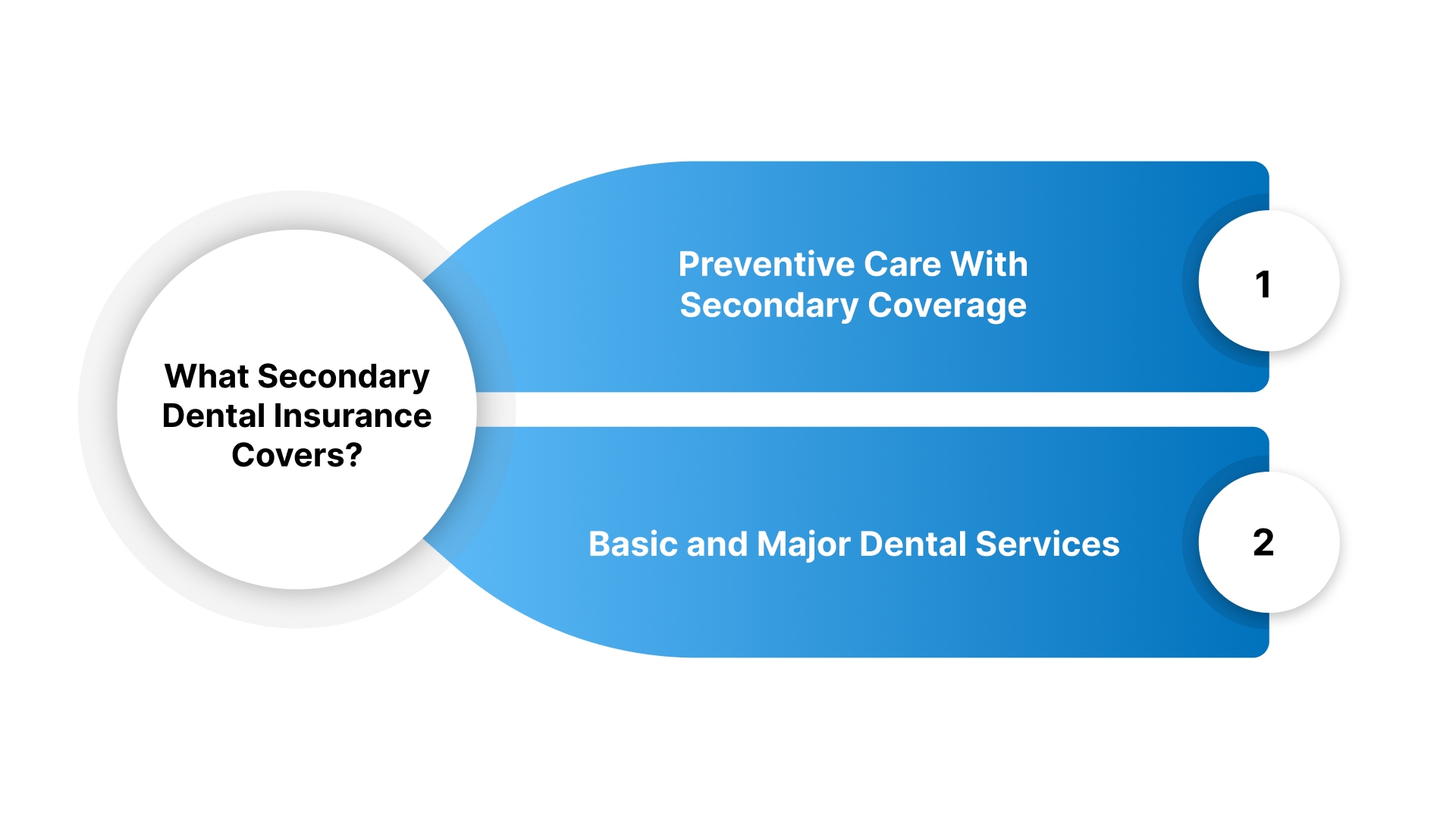

What Secondary Dental Insurance Actually Covers

Secondary coverage typically follows the same benefit categories as your primary plan but focuses on filling in the financial gaps. It provides an extra safety net that becomes active once your first policy has contributed its maximum allowed amount:

Preventive Care With Secondary Coverage

Secondary insurance often covers the remaining cost if your primary plan does not pay one hundred percent for cleanings.

You can sometimes use the second plan if you need more frequent cleanings than your primary plan normally allows.

It is a common misunderstanding that you can get unlimited free cleanings by simply having two separate dental plans.

Basic and Major Dental Services

Secondary plans are very helpful for expensive treatments like fillings, root canals, and porcelain crowns for your teeth.

You can use secondary benefits to continue your treatment if your primary plan hits its annual maximum benefit limit.

You should note that secondary plans will not cover procedures that are explicitly excluded by both of your policies.

Predicting your total savings will help you decide if paying for two separate monthly premiums is worth the cost.

How Much Can Secondary Dental Insurance Save You?

The amount you save depends on the monthly premium costs compared to the additional benefits you receive throughout the year. You should analyze your expected dental needs to ensure that the second plan provides a real financial advantage for you:

Cost Breakdown With One Plan vs Two Plans

Having two plans can significantly lower your bill for major work, but it also means paying two monthly premiums. In some scenarios, the cost of the second premium might be higher than the actual dental savings you receive.

You might experience diminishing returns if both plans have very similar coverage limits and the same list of exclusions.

Annual Maximums and Why Secondary Coverage Helps

Most standard dental plans cap their yearly benefits at a low amount, such as one thousand or fifteen hundred dollars. Secondary coverage provides a second pool of money that you can use once that first annual limit is gone.

This is especially helpful if you need multiple major procedures, such as several root canals or bridges, in one year.

Lowering your out-of-pocket costs is great, but you must still verify if the plan rules align with your needs.

Are you worried about being denied for major work because you have not been on your plan long enough? TrueCost Group provides immediate coverage for root canals, dentures, and gum surgeries with no waiting periods or contracts. Get a free quote over text today to access a plan with up to $5,000 in annual dental benefits.

When to Opt for Secondary Dental Insurance

Dual coverage is not the best solution for everyone, but it offers a massive advantage for those with high needs. You should evaluate your current dental health and your family’s history to see if extra coverage is a wise investment:

Good Use Cases for Secondary Dental Insurance

You know that you need extensive major work like multiple crowns, bridges, or complex periodontal surgeries this year.

Your children require expensive orthodontic treatment like braces, which often exceed the limits of a single dental plan.

You are part of a large family with many dependents who all use their dental benefits regularly for care.

When Secondary Dental Insurance Is Not Worth It

You only visit the dentist for routine cleanings and exams, which are usually covered by your primary plan.

Both insurance policies have identical exclusions and low coverage percentages that do not offer any meaningful extra savings.

The combined cost of the two monthly premiums is more than you would pay for your dental work out-of-pocket.

Avoiding common mistakes during the setup process will ensure that your dual coverage works exactly as you expect.

Common Mistakes With Secondary Dental Insurance

Many patients run into trouble because they do not communicate with both insurance companies or follow the correct filing order. These errors can lead to claim denials and long delays that make your dental visits much more stressful than necessary:

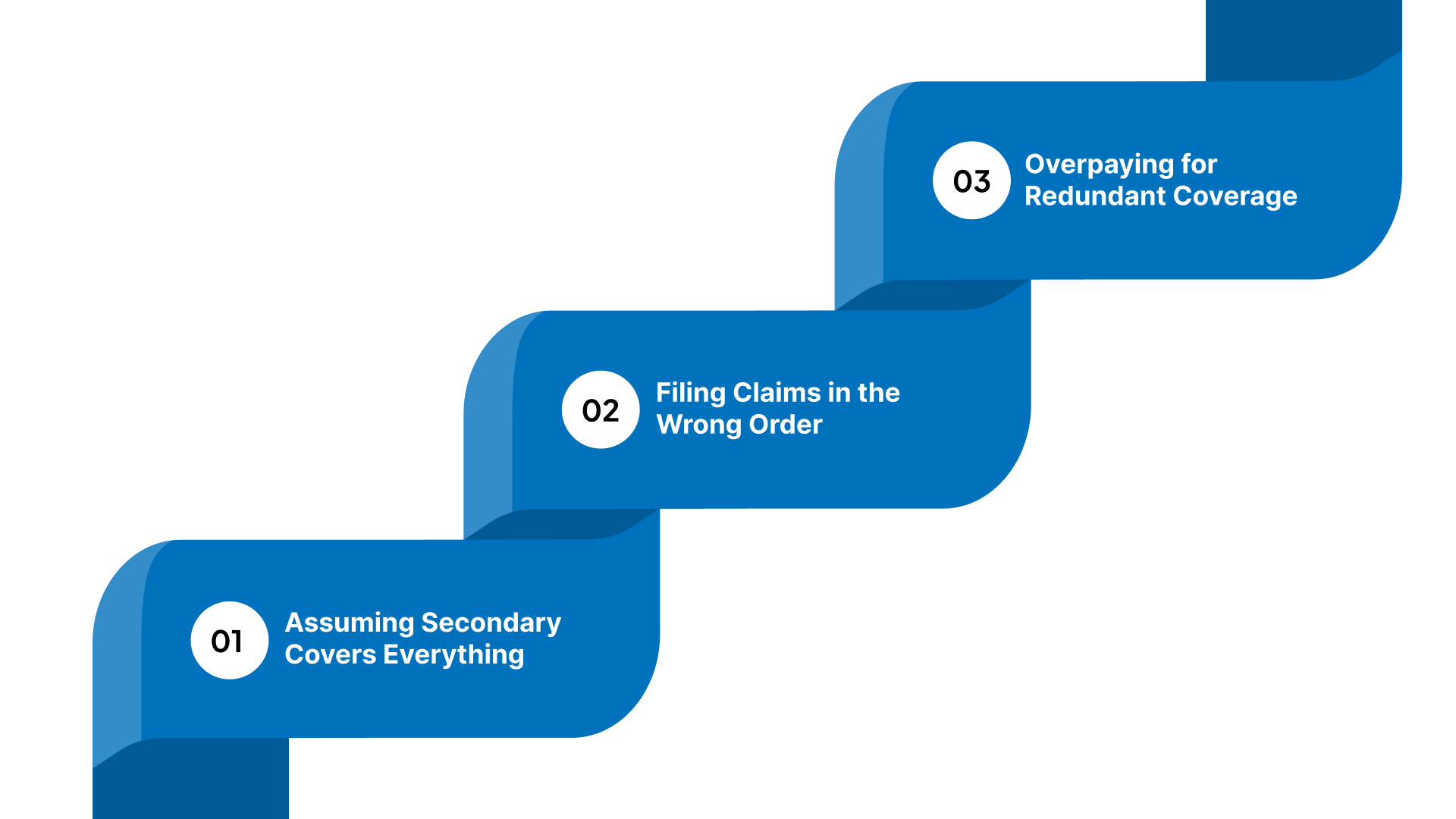

Assuming Secondary Covers Everything

The Mistake: Believing that two plans will always result in a zero-dollar balance for every single dental procedure you receive.

The Reality: You may still face balance billing if your dentist charges more than the allowed amount for both insurance companies.

The Solution: Always ask for a pre-treatment estimate to see how both plans will contribute to your final dental bill.

Filing Claims in the Wrong Order

The Mistake: Submitting your claim to the secondary insurance provider before the primary plan has reviewed and paid its portion.

The Reality: This will cause an automatic denial because the secondary insurer needs the primary EOB to calculate their own payment.

The Solution: Ensure your dental office has your insurance information organized correctly so they submit the primary claim first every time.

Overpaying for Redundant Coverage

The Mistake: Paying for a second private plan that has a high premium but offers very little additional coverage value.

The Reality: Some plans have "non-duplication" clauses that prevent the secondary plan from paying if the primary already paid something.

The Solution: Compare your plan benefit summaries side-by-side to ensure the secondary plan actually fills the gaps in your coverage.

Correctly setting up your plans from the start is the best way to avoid these frustrating and expensive billing errors.

How to Set Up Secondary Dental Insurance Correctly

Setting up dual coverage requires proactive communication between you, your dentist, and both of your insurance providers for success. You must follow a few simple steps to ensure that the coordination of benefits process runs smoothly for every visit:

Step-by-Step Setup Checklist

Confirm which plan is primary by following the standard employment and birthday rules used by all insurance companies today.

Notify both insurance companies that you have dual coverage so they can update your member files with the other information.

Provide your dentist with both insurance ID cards and verify that they are in-network for both of your plans.

Questions to Ask Before Adding a Secondary Plan

"Does this secondary plan have a non-duplication of benefits clause that might limit my total dental insurance payouts?"

"Are there waiting periods for major services on the second plan that would prevent me from using it immediately?"

"Is the provider network for the second plan large enough to include my current family dentist or a local specialist?"

You might also find that simply switching to a better primary plan is a more effective way to save money.

Secondary Dental Insurance vs Other Options

Before you pay for two plans, you should consider whether a single, more robust PPO plan might meet your needs. Comparing your options will help you find the most cost-effective way to keep your teeth healthy without overpaying for insurance:

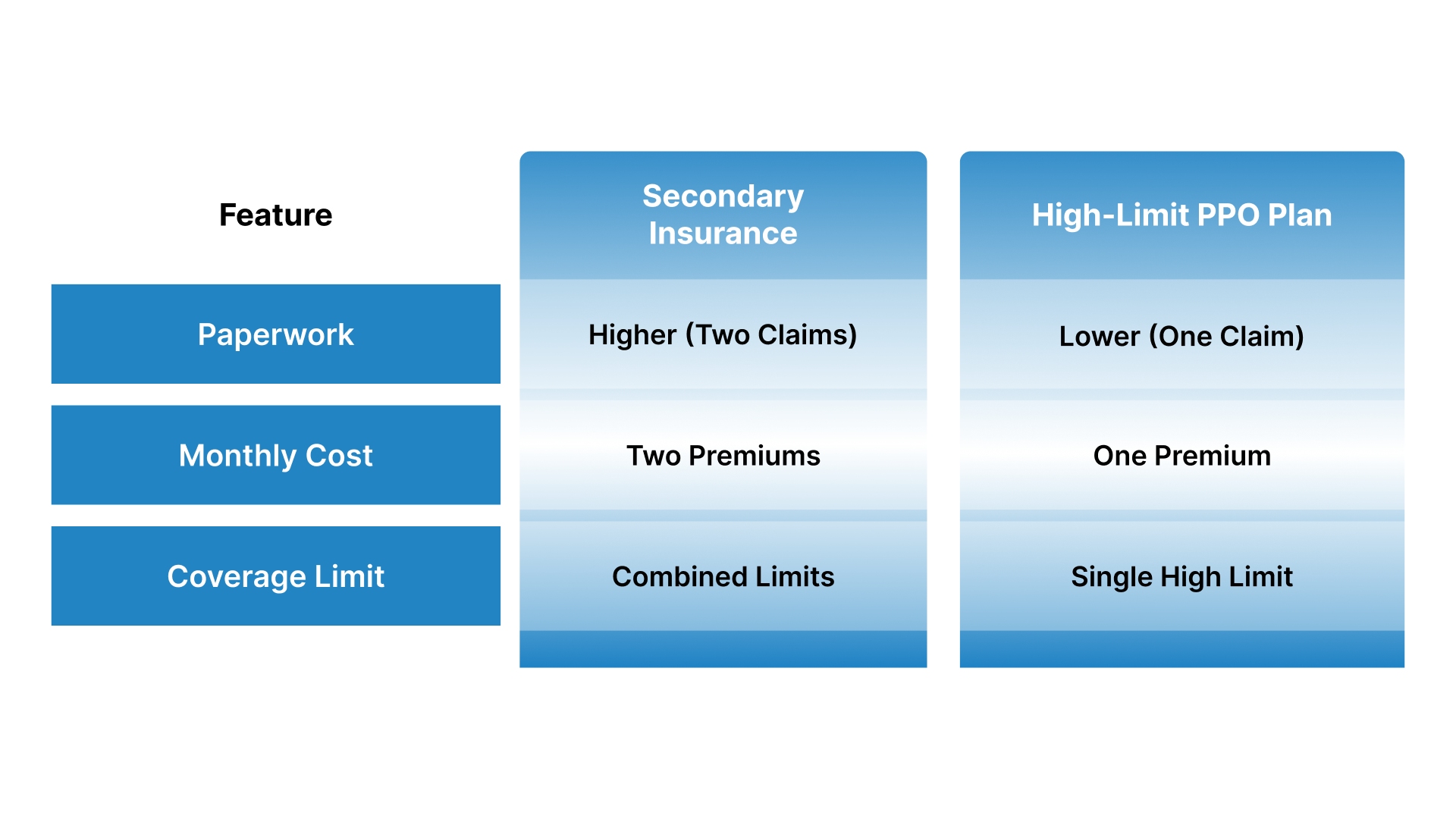

Secondary Insurance vs Better PPO Dental Plan

Adding a second plan can be more expensive than simply choosing one high-quality PPO plan with a larger annual limit. For example, a single plan with a $5,000 limit is often easier to manage than two smaller plans with $1,000 limits.

Feature | Secondary Insurance | High-Limit PPO Plan |

Paperwork | Higher (Two Claims) | Lower (One Claim) |

Monthly Cost | Two Premiums | One Premium |

Coverage Limit | Combined Limits | Single High Limit |

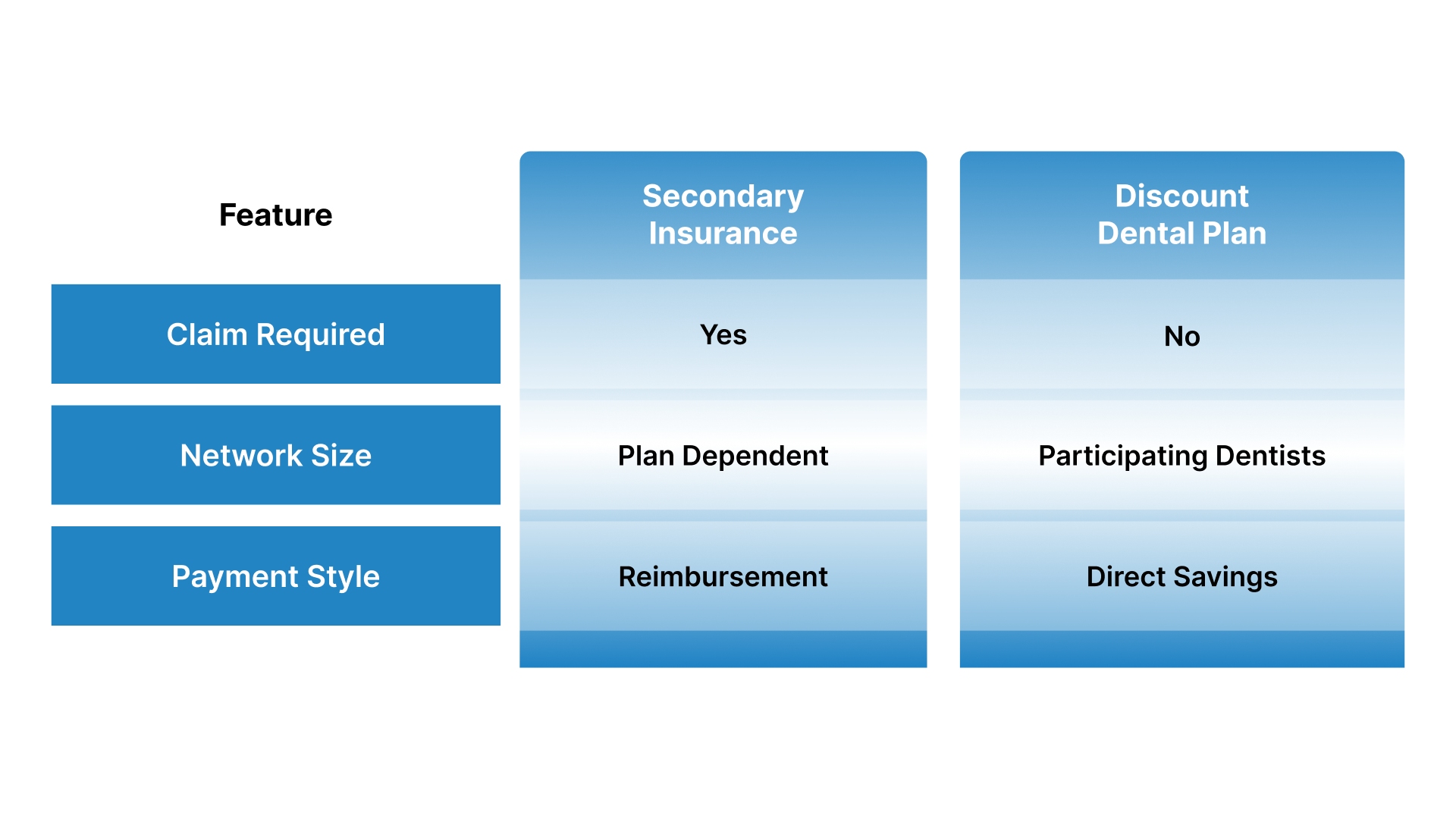

Secondary Insurance vs Discount Dental Plans

Discount plans are not insurance, so they do not coordinate benefits with your primary dental insurance plan in most cases. You usually cannot use a discount plan to pay for the balance that your primary insurance company did not cover.

Feature | Secondary Insurance | Discount Dental Plan |

Claim Required | Yes | No |

Network Size | Plan Dependent | Participating Dentists |

Payment Style | Reimbursement | Direct Savings |

Choosing the right approach will ensure you have the coverage you need when you face an expensive dental procedure.

TrueCost Group: Your Partner for Simple and Affordable Dental Care

Finding the right dental coverage can feel overwhelming when you are managing a tight household budget. Insurance terms and high-limit plans may seem confusing or unreliable. Many families stay uninsured because enrollment feels slow and unclear.

TrueCost Group removes these barriers by helping you access PPO dental plans with clear, high-limit benefits that start immediately. You receive expert guidance through simple messaging so you feel protected before your next dental visit.

High Annual Limits: Access up to $5,000 in yearly coverage to handle major procedures like root canals, crowns, and dentures.

Immediate Protection: You can skip the six-month waiting periods for major work and start your dental treatment on day one.

National Network Access: Choose from over eighty-five thousand dentists who offer deep discounts to lower your total out-of-pocket costs.

Messenger-First Enrollment: Complete your application through WhatsApp or Facebook Messenger to get covered without filling out long, complex forms.

Month-to-Month Flexibility: Manage your budget with a plan that has no long-term contracts and allows you to cancel at any time.

You can finally stop worrying about the high cost of a healthy smile by choosing a plan designed for life.

Conclusion

Secondary dental insurance can be a powerful tool for reducing your bills if you have extensive and expensive dental needs. By understanding how to coordinate your benefits, you can make two plans work together to protect your household budget.

This strategy helps you manage high costs for major procedures and ensures you never have to delay necessary care.

TrueCost Group is here to help you find the best PPO dental options that provide immediate and meaningful financial protection. We specialize in plans that offer high annual maximums and no waiting periods for the major services you need.

Our goal is to simplify your dental insurance experience so you can achieve a healthy smile without the stress.

Get your free quote over text today to see how much you can save on dental care for your family.

FAQs

Q. Can You Have Two Dental Insurance Plans at Once?

Yes, you can legally maintain two dental insurance plans at the same time to increase your total annual benefit limits. The two companies will coordinate their benefits to ensure your total reimbursement does not exceed the actual cost of care.

Q. Does Secondary Insurance Pay After Deductibles?

Secondary insurance usually pays toward your remaining balance after your primary plan has applied its own deductible and coinsurance rules. You must still meet the secondary plan’s deductible if your primary insurance did not already cover that specific dollar amount.

Q. Can Secondary Dental Insurance Reduce My Premiums?

Having a second plan will not reduce the monthly premium of your primary plan and actually increases your total costs. You should only add a secondary plan if the additional benefits for major work are greater than the second premium.

Q. How Do Dentists Know Which Plan Is Primary?

You must tell your dentist which plan is through your own employer and which is through a spouse or parent. They use standard insurance industry rules to designate the primary and secondary plans in their official billing and software systems.

Q. Does Secondary Dental Insurance Affect Claims Speed?

Processing two claims can take longer than filing one because the secondary insurer must wait for the primary plan's response. You can speed up the process by ensuring your dentist has the correct information for both of your insurance policies.