You might feel a sudden sense of panic when you receive a large bill for dental work you thought was covered. It is deeply frustrating to pay monthly premiums only to have your insurance provider refuse to pay for your necessary treatment.

Many families struggle with the unexpected financial burden that comes from a denied claim after a major dental procedure today. You can take specific steps to challenge these decisions and ensure that your insurance company fulfills its professional obligations to you.

Understanding why denials happen allows you to address the root cause and potentially save hundreds or even thousands of dollars. You deserve a clear explanation and a fair path to receiving the dental benefits that you were originally promised.

In this guide, you will learn the exact steps to follow when your dental insurance company refuses to issue a payment.

Quick Look

Identify the Code: Every denial comes with a specific reason code found on your official Explanation of Benefits document for review.

Clerical Errors: Many claims are rejected because of simple typos or incorrect tooth numbers submitted by the dental office staff.

Appeal Deadlines: You typically have between sixty and one hundred eighty days to file a formal appeal after a claim denial.

Pre-Treatment Estimates: Requesting an estimate before your procedure is the best way to verify your coverage and avoid future payment issues.

Professional Guidance: Speaking with a licensed advisor can help you understand complex plan rules that lead to frequent claim rejections.

Why Dental Insurance Sometimes Won’t Pay

Insurance companies follow strict guidelines and internal policies that determine when they will release funds for your dental care services. A refusal to pay does not always mean the treatment was unnecessary, but often indicates a technical or policy violation.

Understanding these underlying causes helps you stay calm while you work through the resolution process with your provider and dentist:

Common Reasons Insurance Refuses Payment

Waiting periods not met: Many plans require you to be a member for six to twelve months before they pay for major work.

Annual maximum already reached: If you hit your yearly benefit limit, the insurer will not pay for any additional dental services today.

Service not covered under the plan: Certain procedures, like cosmetic whitening or adult braces, are often excluded from standard affordable dental insurance policies.

Out-of-network dentist issues: Your plan might only pay for services provided by dentists who have a signed contract with the insurance network.

Coding or documentation errors: Insurance reviewers may deny a claim if the dentist fails to provide current X-rays or the correct procedure codes.

Do you avoid the dentist because you fear a surprise bill for a root canal or an expensive crown? TrueCost Group offers PPO plans with no waiting periods and up to $5,000 in annual coverage for major work. Get a free quote over text today to access 100% free exams and a national network of dentists.

First Things to Do When Dental Insurance Won’t Pay

The moment you realize a claim was denied, you must begin collecting information to build a case for your payment. Taking organized and immediate action ensures that you do not miss any deadlines or lose important documentation required for your appeal:

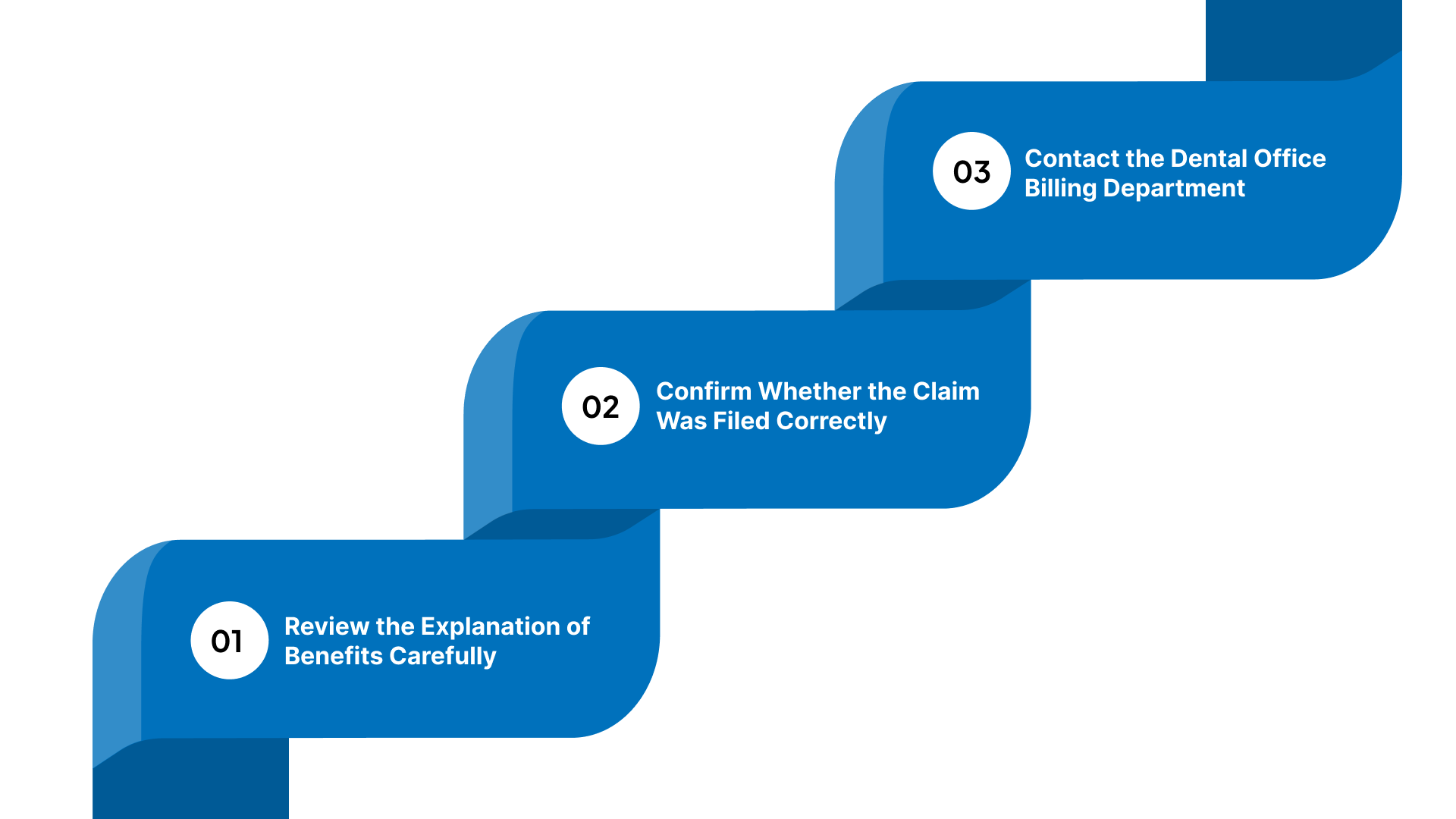

Step 1: Review the Explanation of Benefits Carefully

Look for the specific denial code, which explains the exact reason why the insurance company refused to pay the claim.

Compare the services listed on the EOB to the treatment you actually received at the dental office during your visit.

Check the "patient responsibility" section to see exactly how much the insurance company expects you to pay the dentist yourself.

Step 2: Confirm Whether the Claim Was Filed Correctly

Ask your dentist to verify that the CDT codes used on the claim match the procedure they actually performed for you.

Check for small errors like an incorrect birthdate or a misspelled name that might have caused a system mismatch for payment.

Ensure the office submits the claim to the correct insurance company if you have more than one active dental plan today.

Step 3: Contact the Dental Office Billing Department

Ask the billing coordinator if the insurance company requested additional information, like X-rays or clinical notes that were never sent.

Request that the dental office resubmit the claim if they identify a clerical error that can be easily corrected in the system.

Find out if the office has experience with your specific insurer and can provide advice on how to handle the denial.

Once you have gathered the initial facts, you can determine if the denial is a simple mistake or a final decision.

How to Tell If the Denial Is Legitimate or Fixable

Not every denied claim can be overturned, so you must evaluate the facts to decide if an appeal is worth your time. Some issues are simply a result of the plan rules you agreed to when you first signed up for coverage:

Denials That Can Usually Be Fixed

Missing X-rays or clinical notes: Providing the insurer with the proof they need often results in a quick reversal of the original denial.

Incorrect coding: Fixing a simple administrative error by the dental staff is a very common way to get a claim paid properly.

Network status errors: If a dentist is listed incorrectly in the system, you can often prove their status and get the in-network rate.

Denials That Are Often Final

Cosmetic exclusions: Procedures performed purely for appearance are almost never covered by standard dental insurance plans, regardless of any appeal.

Waiting period violations: If the plan rules state you must wait six months, the insurer is unlikely to pay for work done earlier.

Annual maximum exceeded: Once the insurance company has paid out your full yearly limit, they have no legal obligation to pay more.

Determining the nature of the denial helps you prepare the necessary paperwork if you decide to move forward with a challenge.

How to Appeal a Dental Insurance Claim

An appeal is your formal opportunity to prove that the insurance company should have paid for your dental treatment under your policy. This process requires a structured approach and clear evidence to convince the insurance reviewers to change their original decision for you:

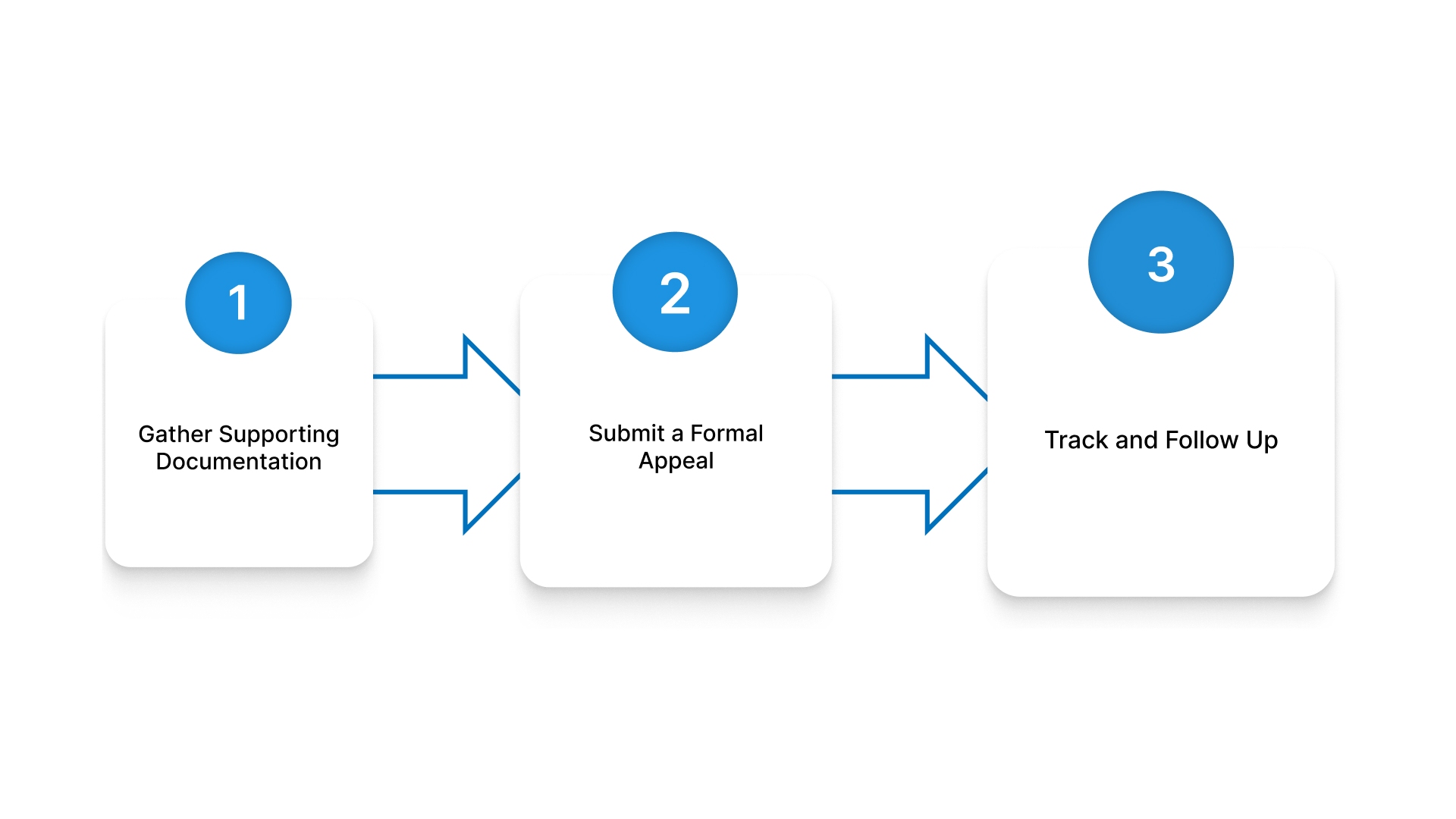

Step 1: Gather Supporting Documentation

Request a copy of the dentist's clinical notes and any X-rays that show why the treatment was a medical necessity.

Ask your dentist to write a brief letter explaining why the specific procedure was the best option for your oral health.

Keep a copy of the original denied claim and the EOB to include with your formal appeal package for the insurer.

Step 2: Submit a Formal Appeal

Write a clear and professional letter that states your name, member ID, and the specific claim number you are currently appealing.

Explain why you believe the denial was incorrect based on your plan's language and the clinical evidence provided by your dentist.

Send your appeal through certified mail or a secure online portal to ensure you have proof of the date it was received.

Step 3: Track and Follow Up

Note the date you submitted the appeal and wait for the standard thirty to sixty days for the insurer to respond.

Call the insurance company's customer service line if you do not receive a written decision within the expected time frame for review.

Prepare to move to a second-level appeal or contact your state's department of insurance if the first appeal is denied again.

If the appeal process does not work, you should look into other ways to manage the balance with your dental provider.

What to Do If Insurance Still Won’t Pay After an Appeal

Even if your appeal is unsuccessful, you still have several ways to lower the final bill and protect your personal financial health. You can work directly with your dental office to find a compromise that fits your budget and covers the remaining costs:

Negotiating With the Dental Office

Asking for self-pay discounts: Many dentists will offer a lower "cash rate" if they know the insurance company will not be paying.

Requesting payment plans: You can often split the remaining balance into smaller monthly payments to avoid a single large and stressful bill.

Adjusting treatment plans: Your dentist might be able to suggest a less expensive alternative for future work to keep your costs down.

Using Secondary or Alternative Coverage

Secondary dental insurance: If you have a second plan through a spouse, they might pay for the portion that the first plan denied.

Discount dental plans: These memberships can provide you with lower rates even for procedures that your traditional insurance plan will not cover.

Flexible spending accounts: You can use pre-tax dollars from an FSA or HSA to pay for the dental work that insurance refused to cover.

Knowing how to handle the final bill can significantly reduce the long-term impact on your family's savings and financial security.

How Much You May Have to Pay and How to Reduce the Damage

The final amount you owe depends on whether your dentist is in-network and what the insurer's allowed rates are for services. You can use several strategies to minimize the financial hit and ensure you are not overcharged for your dental care needs:

Calculating Your Actual Responsibility

Billed amount vs allowed amount: In-network dentists cannot charge you more than the rate the insurance company has officially set for the work.

What insurance already paid: Verify that any partial payments from the insurance company have been correctly applied to your total dental bill.

What remains negotiable: Focus your negotiation efforts on the services that received no coverage at all to get the biggest total discount.

Cost-Reduction Strategies

Spreading treatment across benefit years: You can schedule complex work in December and January to use two different annual benefit limits for payment.

Prioritizing urgent care first: Address the most painful or dangerous issues immediately and delay less critical work until your benefits reset for you.

Asking about alternative procedures: A different type of filling or crown material might be cheaper while still providing the necessary protection for teeth.

Avoiding common mistakes during this process will help you resolve the situation faster and with much less unnecessary emotional stress.

Common Mistakes That Make Denials Worse

Many people make errors during the denial process that end up costing them more money or making the situation harder to fix. Avoiding these pitfalls will help you maintain a professional relationship with your dentist and your insurance company throughout the process:

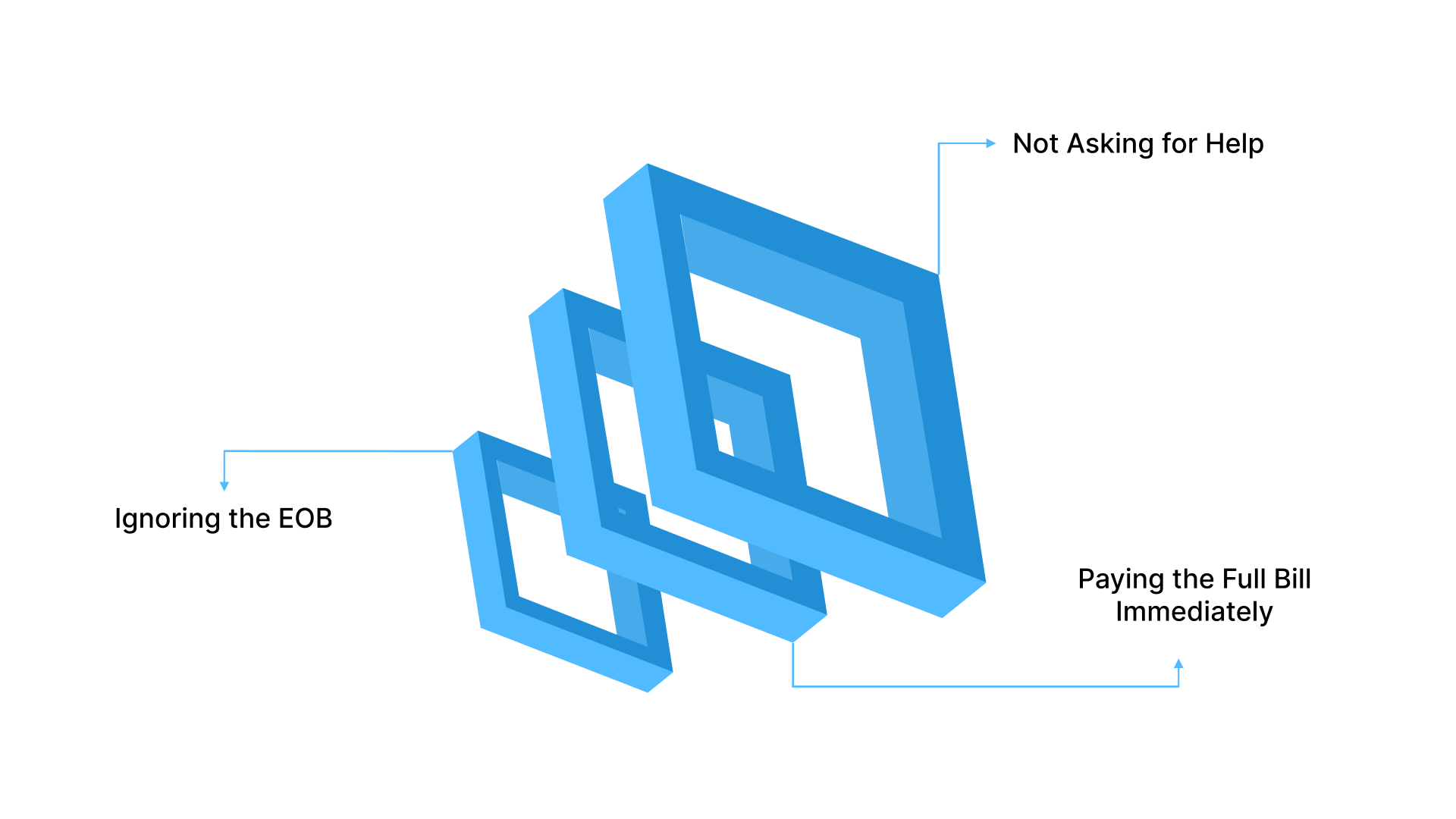

Ignoring the EOB

Failing to read your EOB means you might not realize a claim was denied until you receive a collection notice.

The Solution: Review every piece of mail from your insurance company immediately to catch any payment problems before they escalate further.

Paying the Full Bill Immediately

Paying the dentist's bill right away makes it much harder to negotiate a lower rate if the insurance appeal fails.

The Solution: Inform the dental office that you are appealing the claim and ask them to hold the bill for thirty days.

Not Asking for Help

Trying to understand complex insurance codes alone can lead to frustration and a lack of progress on your claim appeal.

The Solution: Contact a licensed insurance advisor or your HR department to get expert help in navigating the specific plan rules.

Taking a forward-looking approach will help you ensure that you do not face these same insurance problems with your future treatments.

How to Prevent Insurance Denials in the Future

The best way to handle dental insurance rejections is to take proactive steps that ensure your claims are approved on the first try. Being organized and asking questions before you receive treatment will protect you from surprise bills and long appeal processes in the future:

Before Treatment

Requesting pre-treatment estimates: This document tells you exactly what the insurer will pay before you ever agree to the dental work.

Verifying dentist network status: Always confirm that your provider is still in-network before every appointment to avoid paying much higher out-of-network rates.

Checking waiting periods and limits: Review your plan's summary of benefits to ensure you have met all requirements for the work you need.

During Treatment

Confirming procedure codes: Ask your dentist's office which specific codes they plan to use so you can check them against your plan coverage.

Asking about coverage alternatives: If a specific procedure is not covered, ask if there is a similar treatment that the insurer will pay for.

After Treatment

Reviewing claims early: Check your insurance portal a few days after your visit to ensure the claim was filed correctly by the office.

Keeping records organized: Maintain a simple folder with all your EOBs and receipts to make it easier to track your annual maximum usage.

Proper preparation is especially important when you are planning for expensive, major dental work that carries the highest risk of denial.

What to Do When Insurance Won’t Pay for Major Dental Work

Major procedures like crowns and dentures are the most common services to receive a denial because of their high total costs. These cases require extra attention to detail to ensure that you are not left with a bill that you cannot pay:

Root Canals, Crowns, and Dentures

Insurers often deny these claims if they believe a cheaper option, like a simple filling or extraction, was possible for you.

Ensure your dentist provides a clear narrative explaining why the major procedure was the only way to save your natural tooth.

Double-check your coinsurance percentages so you are prepared to pay your fifty percent share of these expensive major dental services.

Emergency Dental Situations

In an emergency, you may not have time for a pre-estimate, but you should still try to find an in-network provider.

Ask the emergency dentist if they can provide a temporary fix until your insurance can verify coverage for a more permanent repair.

Document the date and time of the emergency to prove to the insurer that the treatment could not wait for approval.

TrueCost Group: Your Partner for Simple and Affordable Dental Care

Finding the right dental coverage can feel overwhelming when you are managing a tight household budget. Insurance terms and high-limit plans may seem confusing or unreliable. Many families stay uninsured because enrollment feels slow and unclear.

TrueCost Group removes these barriers by helping you access high-limit PPO dental plans with immediate benefits. You receive expert guidance through simple messaging so you feel protected before your next dental visit.

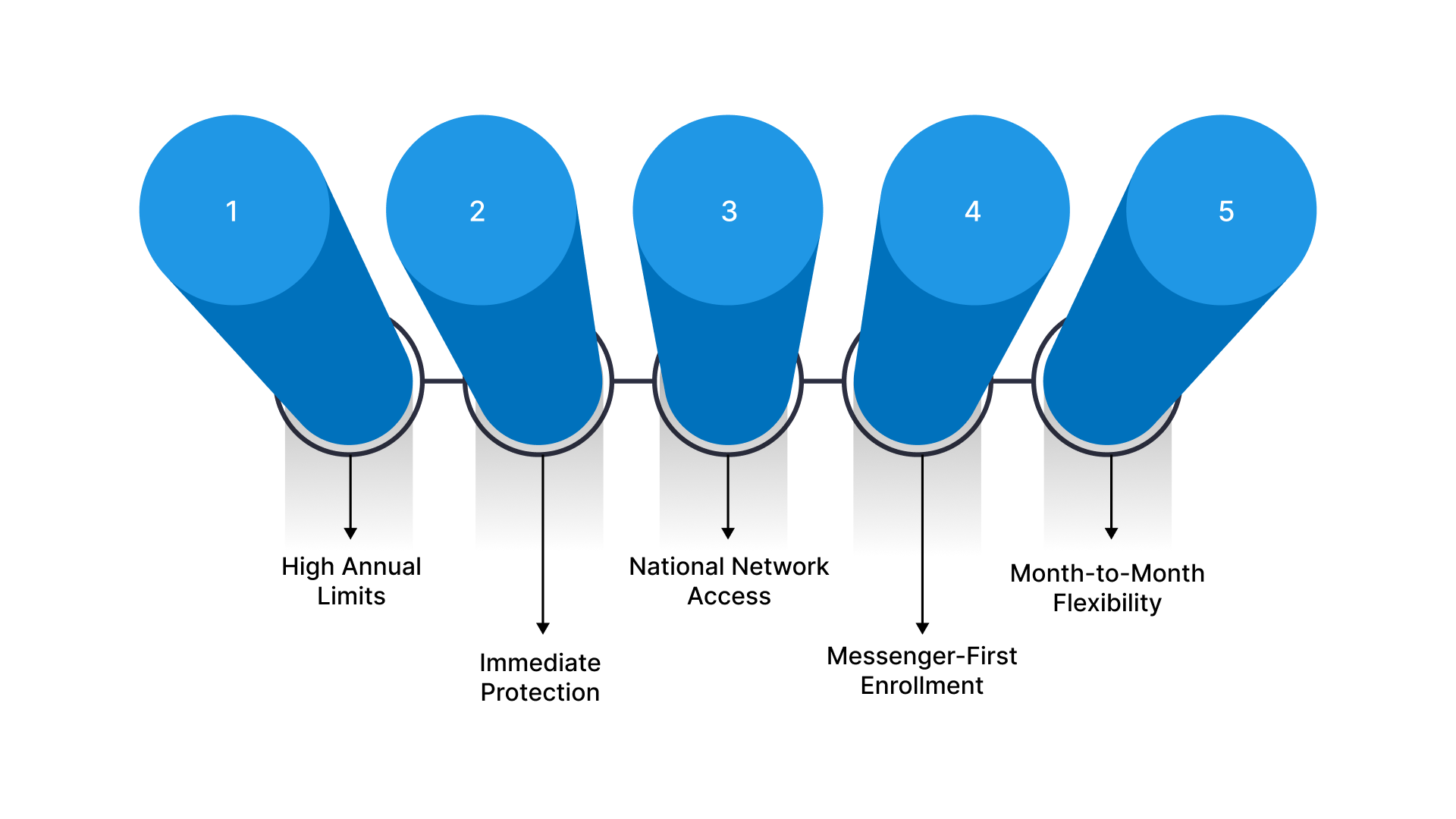

High Annual Limits: Access up to $5,000 in yearly coverage to handle major procedures like root canals, crowns, and dentures.

Immediate Protection: You can skip the six-month waiting periods for major work and start your dental treatment on day one.

National Network Access: Choose from over eighty-five thousand dentists who offer deep discounts to lower your total out-of-pocket costs.

Messenger-First Enrollment: Complete your application through WhatsApp or Facebook Messenger to get covered without filling out long, complex forms.

Month-to-Month Flexibility: Manage your budget with a plan that has no long-term contracts and allows you to cancel at any time.

You can finally stop worrying about the high cost of a healthy smile by choosing a plan designed for life.

Concusion

Dealing with an insurance denial requires patience and a step-by-step approach to identify the specific error or policy rule. Most rejections are fixable if you communicate clearly with your dentist and provide the insurer with the necessary clinical documentation today.

Remember that you have the right to appeal and negotiate to ensure you are treated fairly by your provider.

TrueCost Group is here to help you navigate the complexities of dental insurance so you can focus on your health. We specialize in providing plans that offer clear benefits and high limits to reduce the risk of unexpected claim denials. Our advisors are ready to help you find the protection your family needs to avoid expensive dental billing surprises.

Get your free quote over text today to see how much you can save on dental care for your family.

FAQs

Q. Can Dental Insurance Deny a Medically Necessary Procedure?

Yes, an insurer can deny a necessary procedure if it is not a covered benefit under your specific plan's rules. However, you can appeal the decision by providing clinical evidence from your dentist that proves the treatment was essential for health.

Q. How Long Do I Have to Appeal a Dental Claim?

Most insurance companies give you between sixty and one hundred eighty days from the date of the denial to file. You should check your specific policy or EOB to find the exact deadline to ensure you do not lose your rights.

Q. Should I Pay the Dentist Before Insurance Decides?

It is usually better to wait for the final insurance decision before paying the full bill to avoid overpaying the dentist. You can inform the office that you are appealing the claim, so they do not send your account to a collections agency.

Q. Can a Dentist Change Codes to Get Coverage?

A dentist cannot legally change a code to something that did not happen, as that would be considered insurance fraud today. However, they can use a more accurate code or provide a narrative that better explains the clinical necessity of the work performed.

Q. Does a Denial Affect Future Coverage?

A single denied claim will not impact your eligibility for future coverage or cause your monthly insurance premiums to increase. It only means that the specific procedure was not paid for under the terms of your current active dental insurance plan.