Unexpectedly high dental bills often create confusion, especially when monthly premiums are already being paid. It can feel discouraging to owe additional money for routine treatments like fillings or simple extractions.

Many families struggle to understand why dental insurance does not immediately cover every procedure immediately. Learning how dental deductibles work helps bring clarity to what insurance pays versus what remains your responsibility.

Clear knowledge of these rules makes it easier to plan dental visits and avoid surprises at the front desk. Knowing expected out-of-pocket costs before treatment allows for better financial decisions.

In this guide, you will learn what a deductible is in dental insurance and how to manage these costs effectively.

Quick Look

The Basics: A deductible is a fixed dollar amount you pay for dental services before your insurance company starts paying.

Annual Cycle: Most dental deductibles reset every year on January first, regardless of how much you paid the previous year.

Preventive Waiver: Many PPO plans waive the deductible for cleanings, exams, and X-rays to encourage regular preventive dental care visits.

Cost Range: Typical individual deductibles range between fifty and one hundred dollars for most standard affordable dental insurance plans.

Strategic Timing: Meeting your deductible early in the year can help you save more on major procedures later in that year.

What Is a Deductible in Dental Insurance?

A dental deductible is the specific amount of money you must pay yourself before your insurance benefits become active. It acts as a shared cost between you and the insurer to keep monthly premium prices lower for everyone involved.

Most plans require you to pay this amount once per year for basic or major dental services like fillings. You can think of it as the initial entry fee that unlocks your insurance coverage for the rest of the year.

Knowing how this payment triggers your benefits is essential for calculating your total yearly dental care expenses correctly.

Are you tired of paying high bills because your current plan has a low annual limit or confusing hidden fees? TrueCost Group offers PPO plans with no waiting periods and up to $5,000 in annual coverage for major work. Get a free quote over text today to see how our national network can help your family save.

How a Dental Insurance Deductible Works in 3 Steps

Understanding the timing of your deductible payment helps you manage your household budget without any unnecessary financial stress. The process follows a specific order that determines when your insurance company begins to share the cost of your care:

Step 1: When a Deductible Applies

Deductibles usually trigger when you receive basic services like tooth fillings, simple extractions, or deep cleanings for gum disease.

Most insurance companies also require you to pay the deductible for major work like porcelain crowns or root canal treatments.

You do not typically have to pay a deductible for preventive services like your regular six-month cleanings and oral exams.

Step 2: How You Pay the Deductible

You pay the deductible amount directly to the dental office at the time of your specific dental service or treatment.

The insurance company subtracts the deductible from the total allowed amount of your claim before calculating its own payment portion.

Once you have paid the full deductible amount, you do not have to pay it again for that calendar year.

Step 3: What Happens After the Deductible Is Met

After the deductible is met, your insurance company starts paying its designated percentage for all of your covered dental procedures.

You are then only responsible for your coinsurance, which is a smaller percentage of the total negotiated dental bill.

Your insurance benefits will continue to pay until you reach your annual maximum limit for the current benefit year.

For example, you need a filling that costs $200, and your plan has a $50 annual deductible. You pay the first $50 to meet your deductible, leaving a remaining balance of $150. If your plan covers 80% of fillings, the insurance pays $120, and you pay $30. Your total out-of-pocket cost for this specific filling visit would be $80, including your annual deductible.

Recognizing which specific services require this initial payment will help you prepare for your next visit to the dentist.

What Dental Services Are Subject to a Deductible

Most dental insurance plans divide treatments into different categories to determine if you need to pay your deductible first. Knowing these categories allows you to predict which visits will be free and which ones will require a payment:

Preventive Services and Deductibles

Routine cleanings, annual exams, and bitewing X-rays are the foundation of a healthy smile and good oral hygiene. Many insurance companies waive the deductible for these services to make it easier for you to get preventive care.

This means you can often visit the dentist for a checkup without paying anything toward your annual deductible amount.

Basic Dental Services

Basic services include common dental repairs such as tooth-colored fillings, simple extractions, and emergency treatments for sudden tooth pain. You will almost always have to pay your full annual deductible before the insurance company pays for these services.

This is often the first time during the year that most people realize they have a deductible to pay.

Major Dental Services

Major services include expensive procedures like porcelain crowns, root canals, bridges, dentures, and complex oral or periodontal gum surgeries. Your deductible must be fully satisfied before the insurance company pays its 50% share of these high-cost treatments.

Because major work is expensive, meeting your deductible is a small but necessary step toward receiving your full benefits.

Understanding these service categories helps you estimate the typical ranges for deductibles in most modern dental insurance plans.

How Much Is a Typical Dental Insurance Deductible

The cost of a deductible varies depending on the type of plan you choose and how many people are covered. You should compare these amounts when selecting a plan to ensure the out-of-pocket costs fit within your family budget:

Common Deductible Ranges

Individual deductibles for most PPO plans are very affordable and typically range from twenty-five to one hundred dollars per year. Family plans often have a combined deductible that is capped at two or three times the individual deductible amount.

Once the family limit is reached, no other family members have to pay a deductible for the rest of that year.

Annual vs Lifetime Deductibles

Most dental insurance plans use an annual deductible that resets every year on the first day of your benefit period. Some rare plans may offer a lifetime deductible, which you only pay once as long as you keep the policy.

You should assume your plan resets annually unless your insurance advisor specifically tells you that it is a lifetime option.

Comparing deductibles to other insurance terms like coinsurance and copays will give you a complete picture of your costs.

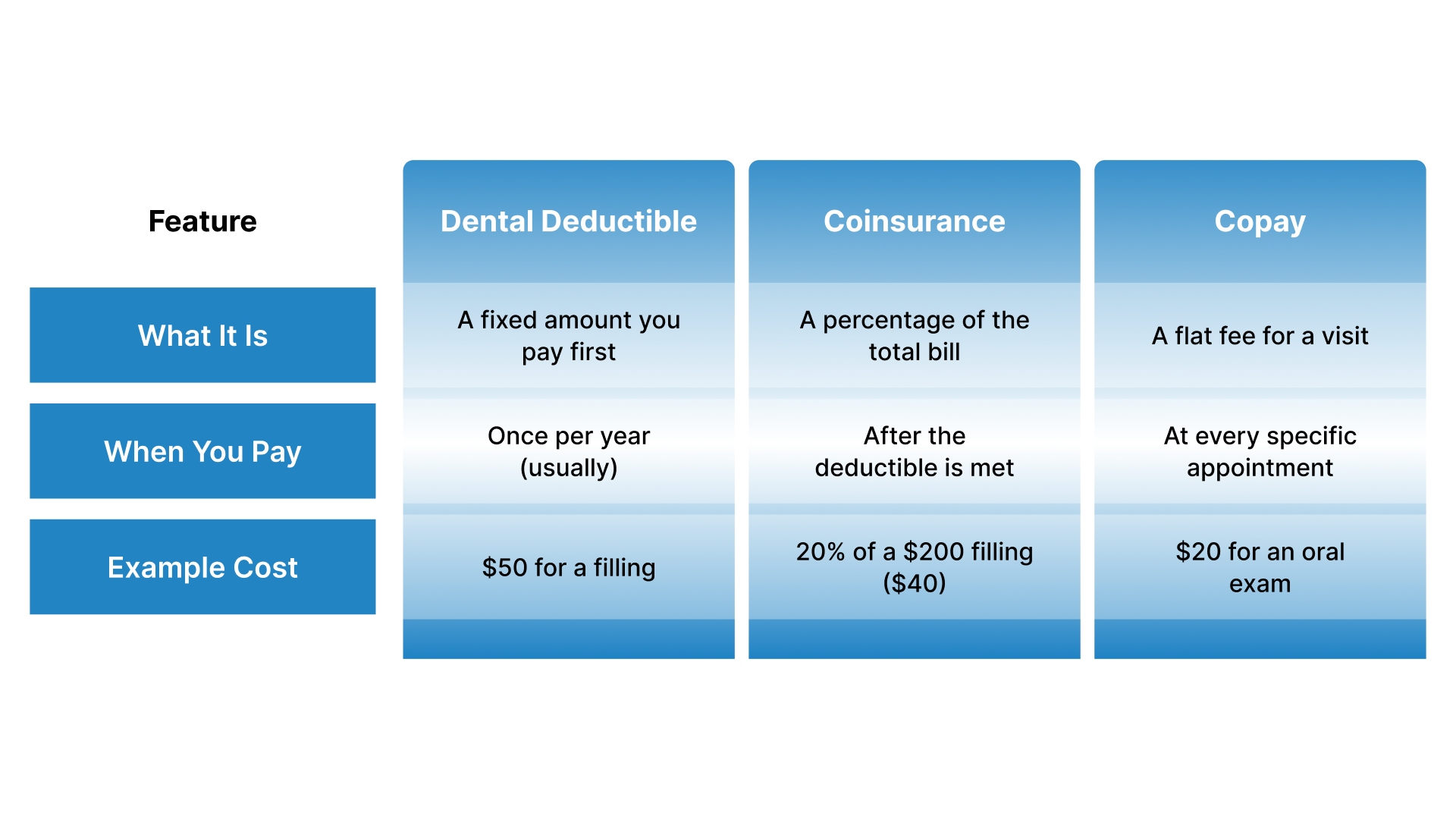

Dental Deductible vs Coinsurance vs Copay

Many people use these terms interchangeably, but they represent very different ways that you share costs with your insurance provider.

Understanding the differences between these three terms is the best way to avoid confusion when reading your dental bills:

Feature | Dental Deductible | Coinsurance | Copay |

What It Is | A fixed amount you pay first | A percentage of the total bill | A flat fee for a visit |

When You Pay | Once per year (usually) | After the deductible is met | At every specific appointment |

Example Cost | $50 for a filling | 20% of a $200 filling ($40) | $20 for an oral exam |

For example, you need a filling that costs $200 at an in-network dentist.

First, your plan has a $50 annual deductible, which you must pay before insurance starts sharing costs. You pay $50, leaving $150 remaining.

Next, your plan uses 20% coinsurance for basic services. Insurance pays 80% of $150 ($120), and you pay 20% ($30).

If your plan also includes a $20 copay for office visits, you pay that amount at checkout.

Total you pay:

$50 deductible + $30 coinsurance + $20 copay = $100

Insurance pays: $120

Knowing how these costs interact is easier when you see how they vary across different types of dental plans.

Are you worried about high out-of-pocket costs because you do not understand how your deductible and coinsurance interact? TrueCost Group simplifies your coverage with affordable PPO plans that offer up to $5,000 in annual benefits and no waiting periods. Get a free quote over text today to access 100% free preventive care and a national network of over 85,000 dentists.

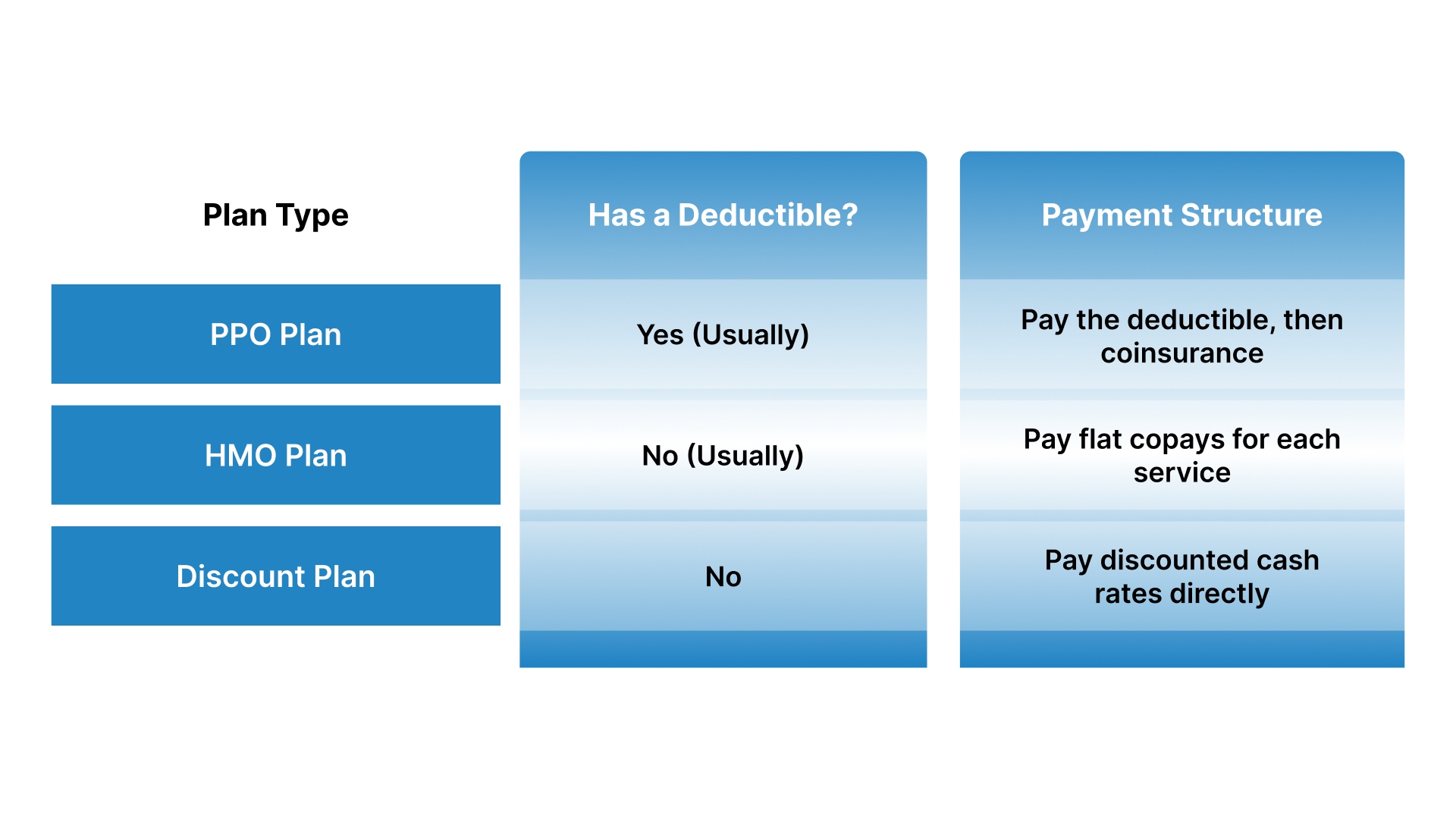

Do All Dental Insurance Plans Have Deductibles?

The presence of a deductible often depends on the type of dental network and the specific structure of the policy.

You can choose a plan with or without a deductible based on how often you expect to visit the dentist:

Plan Type | Has a Deductible? | Payment Structure |

PPO Plan | Yes (Usually) | Pay the deductible, then coinsurance |

HMO Plan | No (Usually) | Pay flat copays for each service |

Discount Plan | No | Pay discounted cash rates directly |

PPO Dental Plans

PPO plans almost always include a small annual deductible that applies to basic and major dental services for the year. This structure gives you the most flexibility to choose any dentist while offering predictable costs through negotiated in-network rates rather than the lowest monthly premiums.

The deductible is a reasonable trade-off for the freedom to visit over eighty-five thousand dentists in a national network and receive partial coverage for major procedures.

HMO Dental Plans

HMO plans often feature $0 deductibles, but they require you to stay within a very small network of specific dentists. You usually pay a fixed copay for every service instead of meeting a deductible and then paying a coinsurance percentage.

These plans are typically the most affordable in terms of monthly cost, making them suitable if you are comfortable with limited provider choice.

Discount Dental Plans

Discount plans are not actually insurance, so they never have deductibles or annual maximum limits for you to worry about. You simply pay the negotiated lower rate directly to the dentist at the time of your specific dental appointment.

This option prioritizes upfront savings over long-term cost protection, especially for major dental procedures.

The way you pay your deductible can also impact how much of your annual maximum benefit remains available for use.

How Deductibles Affect Annual Maximums

Your annual deductible is an out-of-pocket cost that does not count toward your insurance plan's annual maximum benefit limit. For example, if you pay a fifty-dollar deductible, that money is not subtracted from your total yearly insurance allowance.

This is helpful because it leaves more of the insurance company's money available to pay for your expensive procedures. You should always track both your deductible status and your remaining annual maximum to maximize your total dental benefits.

Avoiding common mistakes with your deductible will ensure you get the most value out of your dental insurance plan.

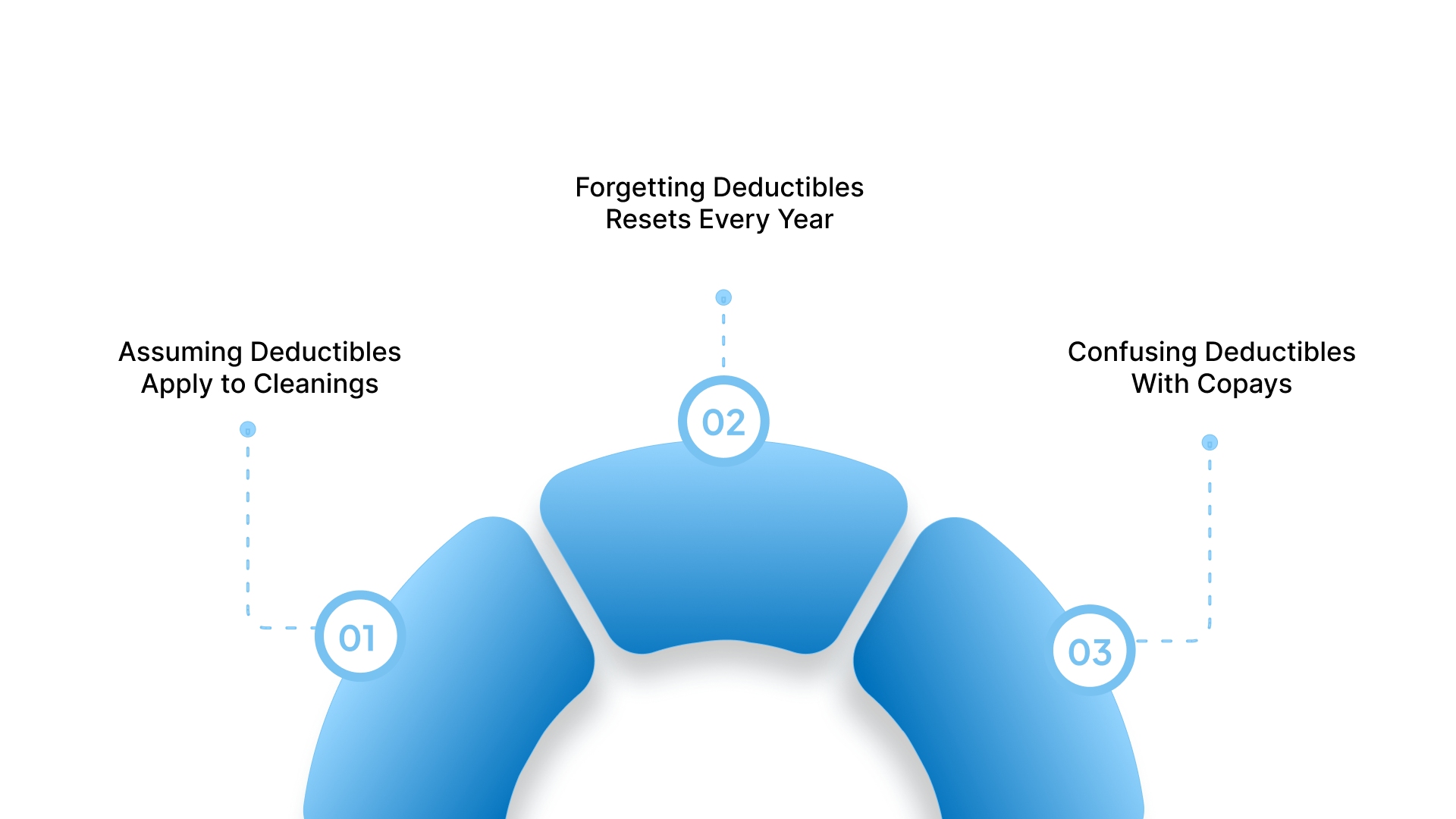

Common Mistakes People Make With Dental Deductibles

Many patients end up paying more than necessary because they do not understand the specific timing and rules of deductibles. Avoiding these common errors will help you save money and reduce the frustration of dealing with dental insurance claims:

Assuming Deductibles Apply to Cleanings

Many people avoid going for their free cleanings because they think they must pay their annual deductible at the visit.

The Solution: Always check your plan summary to see if preventive services are exempt from the deductible before you skip care.

Forgetting Deductibles Resets Every Year

Waiting until the end of December to start a multi-step procedure can result in you paying two separate deductibles.

The Solution: Start major work earlier in the year to ensure you only pay one deductible for the entire treatment process.

Confusing Deductibles With Copays:

Patients are often surprised when a filling costs more than a simple exam because they did not expect a deductible.

The Solution: Ask your dentist for a pre-treatment estimate that clearly shows your deductible and your expected coinsurance for the work.

Using a strategic approach to your dental care can help you meet your deductible in the most cost-effective way.

How to Use Dental Insurance Deductibles Strategically

You can maximize your insurance benefits by planning your dental procedures around the start and end of your benefit year. Taking a proactive approach ensures that every dollar you spend on your deductible works hard to lower your future costs:

Timing Dental Work Wisely

Schedule your basic fillings or extractions early in the year to meet your deductible before you need major work.

If you meet your deductible in June, try to finish all necessary dental treatments before the plan resets in January.

Questions to Ask Before Treatment:

"Has my annual deductible already been fully met by previous dental visits I had earlier this year?"

"Does this specific procedure require me to pay a deductible, or is it covered at one hundred percent?"

When a Higher Deductible Might Make Sense:

Choosing a plan with a higher deductible often leads to much lower monthly premiums for your family.

This is a great strategy if you only plan to use your insurance for free preventive cleanings and exams.

Planning ahead is much easier when you have a dental insurance provider that offers clear and immediate benefits for families.

TrueCost Group: Your Partner for Simple and Affordable Dental Care

Finding dental coverage can feel overwhelming when you are managing a tight household budget and confusing insurance terms. Many families stay uninsured because enrollment feels slow, unclear, and filled with hidden costs.

TrueCost Group simplifies this process by helping you access high-limit PPO plans with clear, immediate benefits. You receive affordable coverage that starts working from day one, along with expert guidance through simple messaging before your next dental visit.

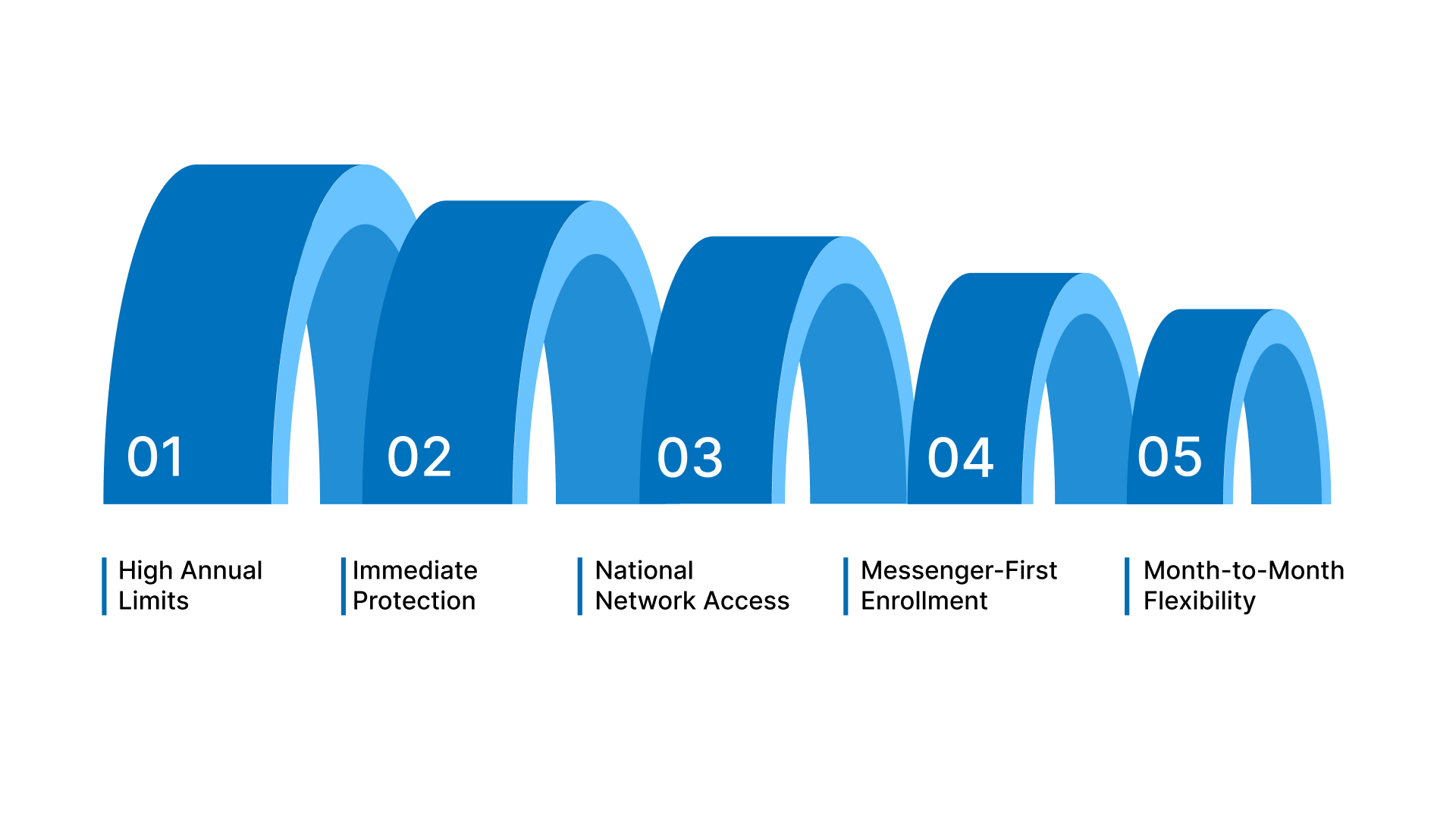

High Annual Limits: Access up to $5,000 in yearly coverage to handle major procedures like root canals, crowns, and dentures.

Immediate Protection: You can skip the six-month waiting periods for major work and start your dental treatment on day one.

National Network Access: Choose from over eighty-five thousand dentists who offer deep discounts to lower your total out-of-pocket costs.

Messenger-First Enrollment: Complete your application through WhatsApp or Facebook Messenger to get covered without filling out long, complex forms.

Month-to-Month Flexibility: Manage your budget with a plan that has no long-term contracts and allows you to cancel any time.

You can finally stop worrying about the high cost of a healthy smile by choosing a plan designed for life.

Conclusion

Understanding what a deductible in dental insurance is the key to managing your family's overall oral health costs. By knowing which services require a deductible, you can avoid surprise bills and plan your dental treatments more effectively.

Remember that meeting your deductible is a small investment that unlocks significant savings for the rest of your benefit year.

TrueCost Group is dedicated to helping you find affordable PPO dental plans that offer clear benefits and high annual limits. We simplify the insurance process so you can focus on your health instead of worrying about confusing medical billing terms.

Our team is ready to help you find a plan that fits your budget and provides the protection you need.

Get your free quote over text today to see how much you can save on dental care for your family.

FAQs

Q. Is a Dental Deductible Paid Every Visit?

No, you typically only pay your dental deductible once per year for the first non-preventive service you receive at the dentist. Once the full deductible amount is met, the insurance company pays its share for all other covered visits that year.

Q. Does the Deductible Apply to Preventive Care?

Most modern dental insurance plans waive the deductible for preventive services like cleanings, oral exams, and basic diagnostic X-rays. This allows you to maintain your oral health through regular checkups without any initial out-of-pocket deductible costs for you.

Q. Does a Family Deductible Work Differently?

A family deductible caps the total amount the entire family must pay before the insurance company covers everyone at the full rate. Once two or three family members meet their individual deductibles, the deductible is considered met for every person on the plan.

Q. What Happens If I Never Meet My Deductible?

If you only go for free preventive cleanings, you may never need to pay your annual deductible during the benefit year. The deductible only matters if you require basic or major dental work like fillings, crowns, or extractions for your teeth.

Q. Can a Deductible Be Waived?

Insurance companies usually only waive deductibles for preventive care to encourage patients to seek early treatment and maintain their health. You can find plans with $0 deductibles, but these often come with higher monthly premiums or a more restricted network.